Visa and Brale test whether privacy-preserving stablecoin rails can fit institutional settlement

Visa’s latest Canton pilot pushes stablecoin settlement deeper into institutional market structure, focusing less on consumer crypto payments and more on privacy, compliance and programmable cash.

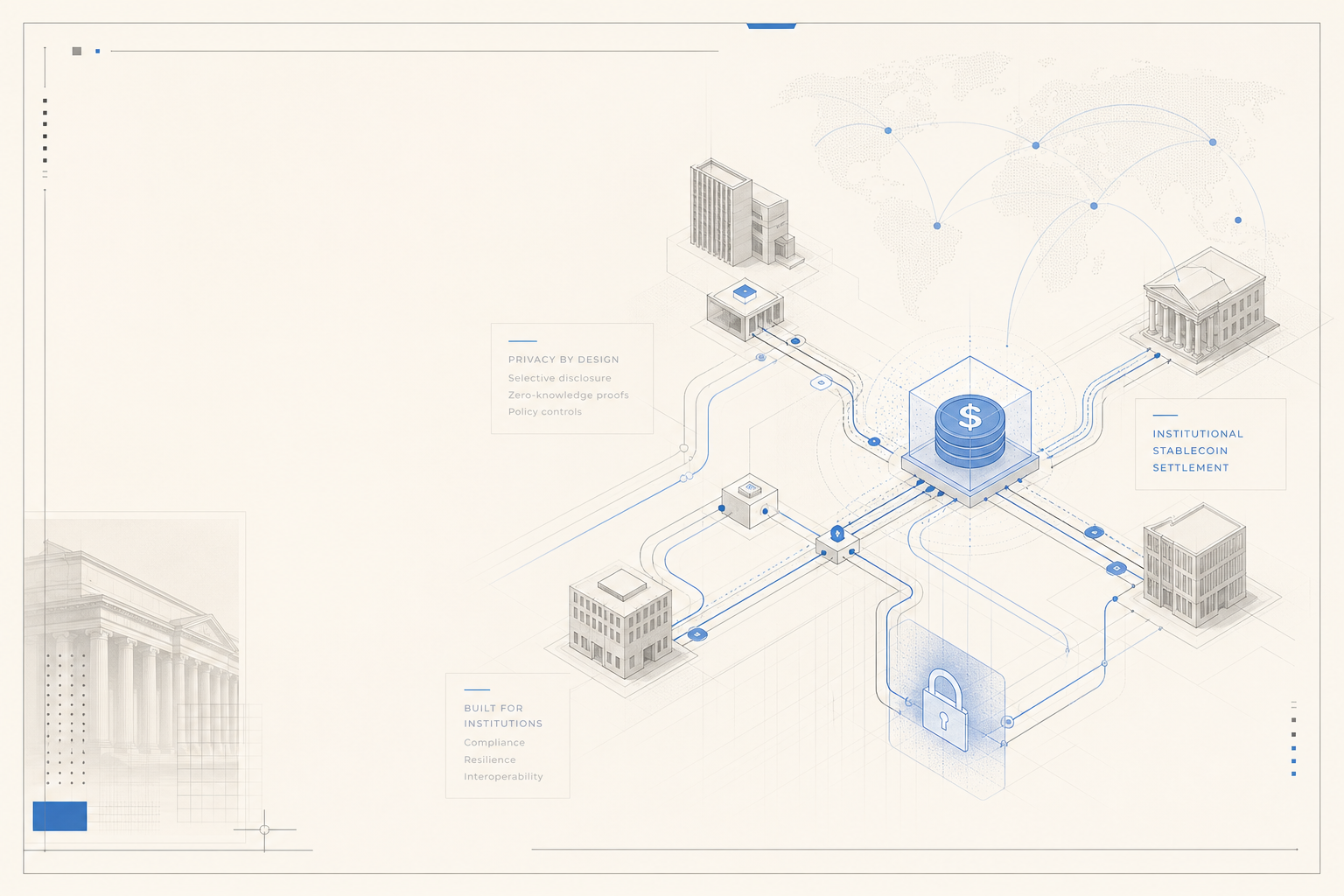

Visa’s newest stablecoin experiment is less about headline-grabbing crypto payments and more about a harder institutional problem: whether digital dollars can move through regulated financial workflows without exposing sensitive transaction data. In a proof of concept with stablecoin infrastructure firm Brale and the Canton Network, Visa is testing settlement flows built around SBC, a dollar-backed stablecoin, to see whether privacy-aware blockchain rails can support institutional payments while preserving the controls banks, payment providers and market infrastructure operators expect. The project stands out because it shifts the conversation from stablecoins as internet-native money to stablecoins as back-end financial plumbing.

The structure of the pilot is straightforward but strategically important. Brale’s SBC stablecoin is being used to simulate institutional payment and settlement activity on Canton, while Visa evaluates whether that token could eventually sit alongside the stablecoins already used in its broader settlement work. The point is not simply to prove that another dollar token can settle onchain. It is to test whether programmable money can move across a network where transaction visibility is tightly scoped, rather than broadcast in the open as it would be on a conventional public chain. For institutions handling treasury flows, cross-border obligations, collateral movements or tokenized-asset settlement, that privacy requirement is often the difference between a workable design and a non-starter.

That is where Canton’s architecture matters. Canton positions itself as a public blockchain network built for regulated markets, with a “need-to-know” privacy model and a synchronizing layer that allows separate applications to interoperate without making all underlying data universally visible. Its own stablecoin-payments materials describe a network already connected to trillions of dollars in tokenized assets and designed for tokenized cash, real-time settlement and compliance-sensitive financial applications. In practice, that means participants can pursue atomic settlement and round-the-clock programmability while still limiting who can see counterparties, pricing details, positions and cash movements. For traditional financial institutions, that is a far more relevant proposition than consumer-facing payment demos on fully transparent rails.

Brale’s role adds another useful signal. In its own Canton announcement, the company said businesses in supported US states will be able to mint and redeem stablecoins on Canton one-for-one using USDC, USDP and PYUSD across more than ten blockchain networks as well as wire and ACH rails. Brale also says SBC is fully backed by cash, cash equivalents and short-term US government bonds held at US financial institutions, with monthly third-party reserve attestations. Those details matter because the institutional case for stablecoins depends on more than transfer speed. Issuers have to show redeemability, reserve quality, operational interoperability and a pathway into the existing fiat system. Without that, tokenized cash remains a closed-loop product rather than a settlement instrument.

Visa is also not entering this market cold. The company has been experimenting with stablecoin settlement since 2021, when it began using USDC on Ethereum to settle certain payment flows. What changes in this pilot is the target environment. Earlier public-chain work demonstrated that stablecoins could help compress settlement timelines. The Canton test asks a more specific next-stage question: can the same logic be adapted for institutions that want blockchain efficiency but cannot accept full public transparency around transaction data? As tokenized deposits, tokenized money market funds and other cash-like instruments spread through wholesale finance, that question becomes central to whether stablecoins remain mostly crypto-native tools or become part of mainstream institutional operations.

The broader market backdrop makes the timing credible. Stablecoin issuance has already moved well beyond experimental scale, but much of the volume still serves trading activity. The next leg of growth depends on getting stablecoins into business payments, treasury management, cross-border settlement and capital-markets workflows. That requires legal clarity, better controls and infrastructure that can connect tokenized cash to other tokenized financial assets. Canton and Brale are both explicitly aiming at that crossover point. Their public materials frame stablecoins not as standalone crypto products, but as cash components inside a wider onchain financial stack that includes financing, collateral mobility, liquidity routing and real-world assets.

The proof of concept does not guarantee production deployment, and it does not settle harder questions around standards, regulation or commercial adoption. But it does show where the institutional stablecoin market is going. The frontier is no longer just whether a payment can clear onchain; it is whether onchain cash can meet the privacy, interoperability and governance requirements of large financial actors. If that threshold is crossed, stablecoins start to look less like an alternative payments novelty and more like a serious settlement layer for the tokenized financial system that banks, networks and issuers are now trying to build.