Visa Pushes Deeper Into Stablecoin Settlement as It Builds the Agentic Commerce Stack

Visa used its Payments Forum to tie together AI checkout tooling, broader stablecoin settlement coverage and more card-linked digital dollar distribution. The move shows how large payment networks are positioning stablecoins less as a retail novelty and more as programmable settlement infrastructure.

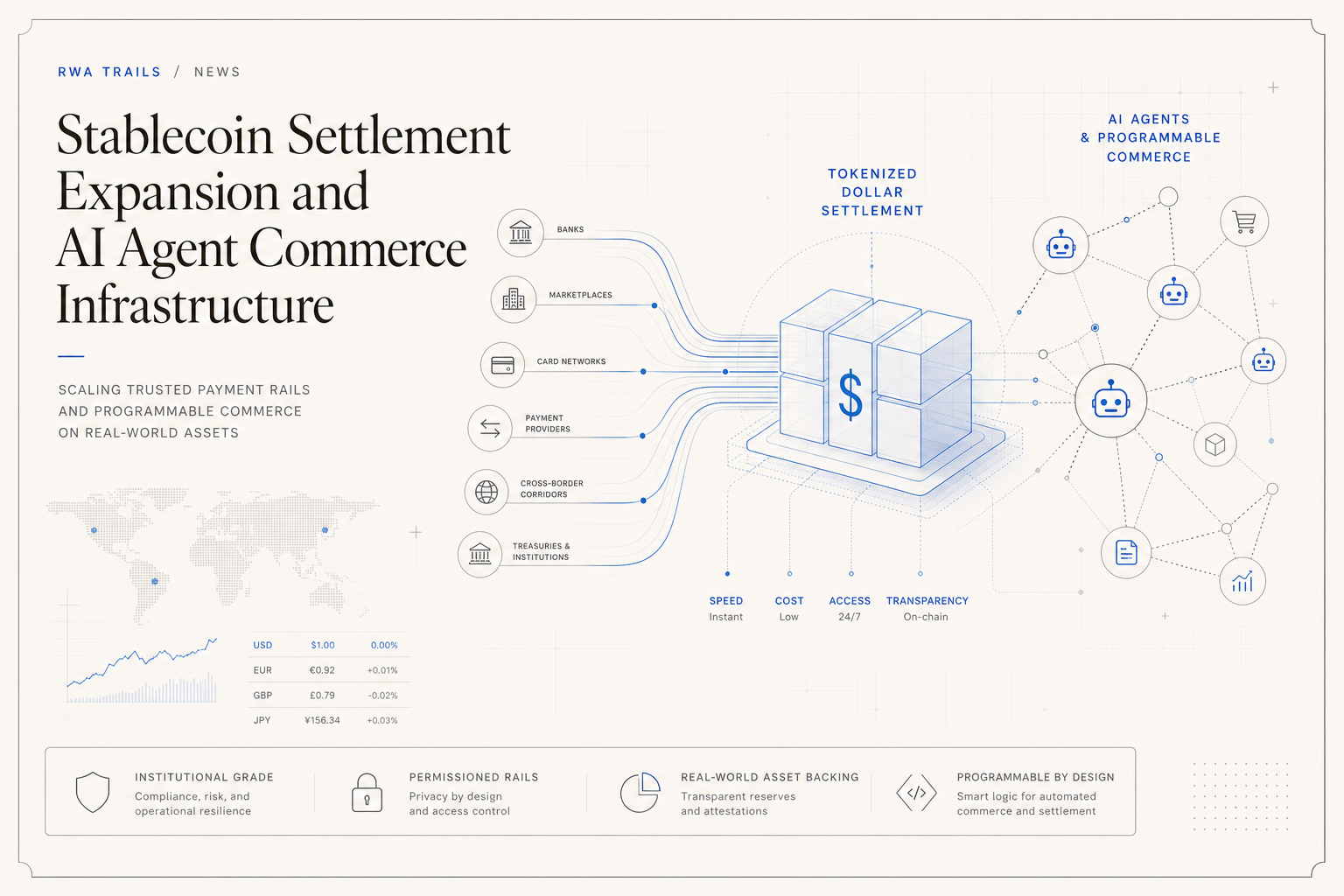

Visa is widening its stablecoin strategy from a narrow crypto settlement experiment into a broader commerce infrastructure push that now spans AI-initiated payments, tokenized deposit concepts, card distribution and multi-chain settlement. At Visa Payments Forum 2026, the company presented that stack as a coordinated product roadmap rather than a series of disconnected pilots. That matters for RWA markets because it frames tokenized dollars as operational plumbing for large-scale commerce, not just an exchange on-ramp or treasury instrument.

The immediate announcement combined several layers. On the front end, Visa introduced merchant and risk tools for agentic commerce, including Agent Score, Agentic Directory and a Large Transaction Model aimed at fraud and authorization performance. It also said OpenAI will work with Visa to support secure payments initiated by AI agents. On the back end, Visa said it is expanding stablecoin settlement pilots across more regions, blockchains and currencies while also extending the range of stablecoin-linked card programs that can connect digital asset balances to ordinary card acceptance.

The significance is less about any single product label than about the architecture Visa is describing. The company is effectively trying to preserve its role at the trust, routing and compliance layer while new forms of money move underneath. In that model, merchants do not need to become stablecoin specialists, banks do not need to abandon deposits, and developers do not need to rebuild global acceptance from scratch. Tokenized dollars and tokenized bank liabilities become new settlement formats, while Visa remains the orchestration layer connecting wallets, issuers, acquirers and merchant checkout flows.

Visa's earlier disclosures this year help show that the latest announcement is not a greenfield concept. In late April, the company said it was adding five more blockchains to its stablecoin settlement program — Arc, Base, Canton, Polygon and Tempo — alongside the four networks it had already been supporting: Avalanche, Ethereum, Solana and Stellar. Visa also said the pilot's annualized stablecoin settlement run rate had climbed 50% over the prior quarter to $7 billion. Those figures do not make stablecoin settlement a dominant share of global card volume, but they do show that the program is moving beyond symbolic experimentation and into measurable operational usage.

The distribution side is also becoming clearer. In March, Visa and Bridge said they were working to expand stablecoin-linked card programs to more than 100 countries across Europe, Africa, the Middle East and Asia Pacific by year-end, building on earlier launches in 18 nations. The same announcement tied those cards to on-chain settlement through Lead Bank and to Visa's broader stablecoin settlement pilot. Taken together with this week's product updates, that suggests Visa is constructing a loop in which stablecoins can be issued or funded through fintech partners, spent through ordinary card rails, and settled on supported blockchains without forcing end users to manage the mechanics directly.

For RWA operators, the practical implication is that stablecoins are increasingly being treated as settlement infrastructure for programmable finance rather than as a standalone product category. That opens room for tokenized treasury products, on-chain cash management tools and other yield-bearing dollar instruments to plug into a payment environment that already has distribution and merchant acceptance. If a payment network can normalize stablecoin settlement windows, support cross-chain optionality and pair that with tokenized deposits from banks, the path from tokenized asset ownership to real-world spending or treasury operations becomes much shorter.

The OpenAI angle adds a second layer of relevance. Agentic commerce only scales if the payment instruction, risk check and final settlement all happen inside a trusted framework. Visa's position is that AI agents may become legitimate economic actors for consumer and business purchasing, but they will need credentialing, transaction controls and dispute-ready payment rails to do so safely. Stablecoins fit that thesis because they can move continuously across digital infrastructure, while the network and issuer layer can still apply policy, fraud controls and account-level permissions.

There are still meaningful limits. Visa did not disclose transaction volumes by corridor, the currencies beyond dollars that may be added next, or the commercial terms that will determine whether banks and fintechs adopt tokenized deposits at scale. Stablecoin settlement also remains subject to jurisdiction-specific policy treatment and counterparty preferences. Even so, the company's latest announcements point in one direction: large incumbents no longer appear to be evaluating stablecoins only as a crypto adjacency. They are increasingly designing for a world in which tokenized cash, card acceptance and AI-driven transaction initiation sit inside the same production payments stack.