Sanctioned Iran Wallet Freeze Shows How Stablecoin Compliance Now Operates in Real Time

A new U.S. sanctions update added four TRON wallets tied to Iran’s central bank, and Tether froze about $131 million in USDT linked to those addresses. The episode shows how stablecoin settlement infrastructure can become an immediate enforcement layer for cross-border financial controls.

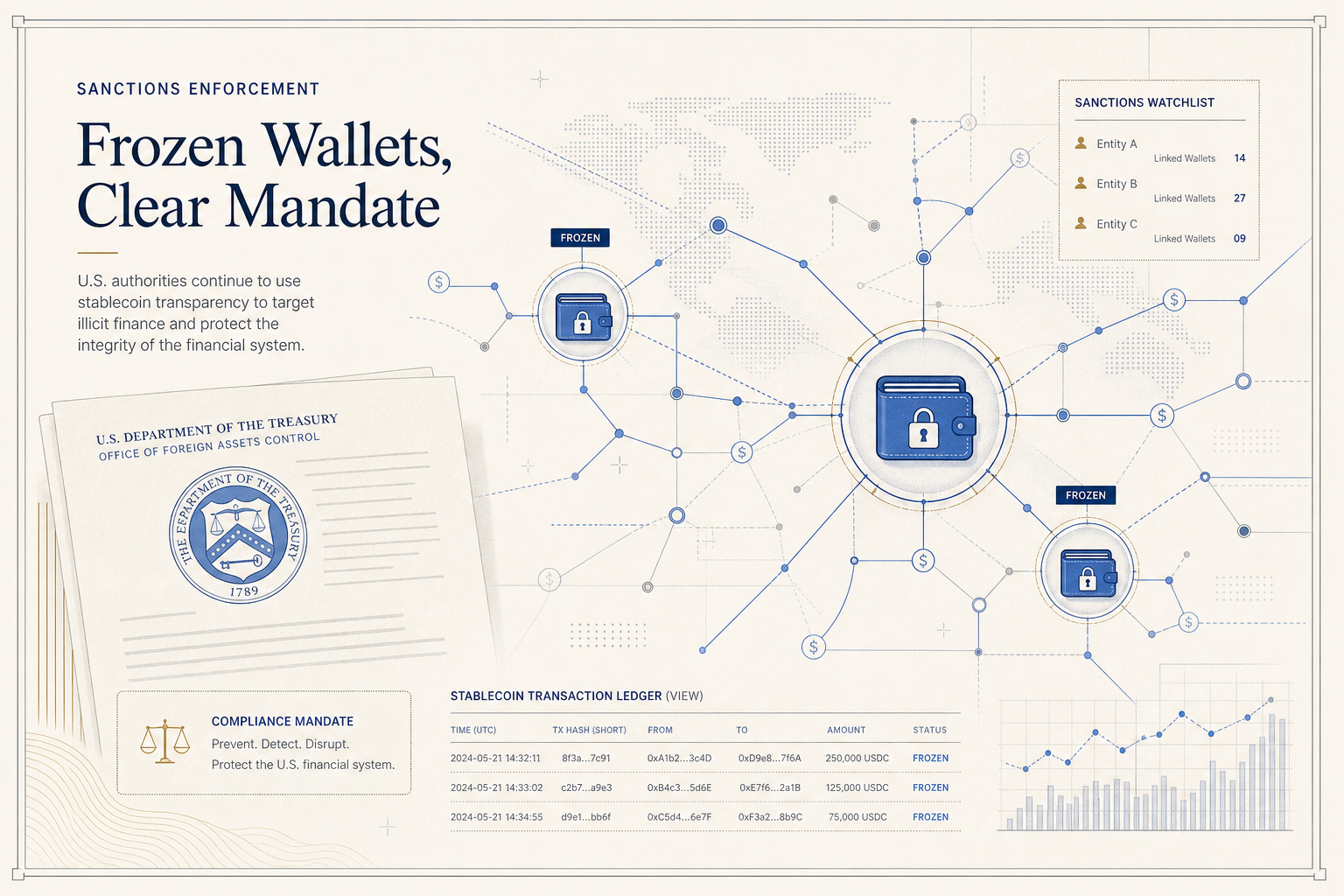

A mid-July U.S. sanctions update has turned into a live demonstration of how stablecoin compliance works when regulators, public wallet identifiers and issuer controls intersect. The Office of Foreign Assets Control updated the designation for Iran’s central bank to include four additional TRON addresses, and roughly $131 million in USDT associated with those wallets was subsequently frozen. For RWA and stablecoin markets, the significance is larger than the headline amount: it shows that dollar-backed tokens are no longer just payment instruments or trading collateral, but increasingly a programmable enforcement surface inside the broader financial system.

The mechanics matter. OFAC’s published update added four more digital currency identifiers to the existing sanctions record for Bank Markazi Jomhouri Islami Iran, the Central Bank of Iran. Public blockchain analysis released around the designation found that the newly identified addresses had received more than $165 million in stablecoins, while only about $131 million remained available to be immobilized by the time the freeze took effect. That gap is a reminder that sanctions designations still move on human and institutional timelines, while funds on public chains can shift quickly across addresses, intermediaries and counterparties before a freeze is executed.

The U.S. government’s position on the institution itself is not new. Treasury sanctioned Iran’s central bank in 2019 under counterterrorism authorities, tying the designation to support for the IRGC-Qods Force, Hezbollah and other regional actors. What has changed is the operational expression of that policy. Instead of stopping at named entities and conventional banking touchpoints, enforcement is now extending directly into specific blockchain addresses that can be screened by exchanges, custodians, payments firms and stablecoin issuers almost immediately after publication. In practice, that makes the sanctions perimeter more machine-readable than in earlier crypto enforcement cycles.

The stablecoin angle is especially important. Unlike bearer cash or self-custodied assets without issuer-level controls, centrally issued dollar tokens can often be frozen at the contract or administrative layer once a wallet is identified as blocked property. That feature has always been part of the policy debate around fiat-backed stablecoins, but episodes like this convert the abstract debate into operating reality. If a regulator publishes wallet identifiers and the issuer acts, stablecoin balances can become economically inert even though the tokens remain visible onchain. The assets are not seized in the conventional sense, yet they can no longer move or redeem through the issuer.

That matters for institutions building around tokenized cash and tokenized assets. Many RWA transaction stacks rely on stablecoins as the settlement leg for subscriptions, distributions, collateral transfers and treasury movements. The same characteristics that make these instruments useful for capital markets infrastructure — continuous transferability, transparent ledgers and issuer-managed redemption — also make them easier to plug into compliance workflows than many earlier forms of crypto liquidity. This case reinforces that stablecoin infrastructure is evolving as a regulated financial rail, not merely an adjacent crypto convenience layer.

It also highlights a strategic asymmetry inside the market. Public blockchains offer traceability, but enforcement still depends on whether key intermediaries can act on that visibility. In this instance, the combination of an official sanctions update and issuer controls appears to have converted address-level attribution into a practical freeze. That is a meaningful signal for banks, payment companies and tokenization platforms evaluating which digital-dollar models are compatible with compliance-heavy use cases. The more important stablecoins become in commercial settlement, the more their governance and freeze mechanics become part of product due diligence rather than a footnote for legal teams.

There is a second-order implication as well. OFAC notes that listed wallet identifiers are not necessarily exhaustive, which means counterparties cannot treat a published address list as a complete map of exposure. Compliance programs still need transaction monitoring, counterparty screening and escalation processes that extend beyond static deny lists. For stablecoin issuers and institutional users, that raises the bar from simple sanctions screening toward continuous risk operations, especially when flows can move across chains, service providers and offshore venues before enforcement catches up.

For the RWA sector, the lesson is straightforward. Stablecoins are becoming embedded in the same control architecture that governs mainstream cross-border finance, and their credibility with institutions will increasingly depend on that integration. The latest Iran-related freeze does not settle every debate around sanctions, issuer discretion or censorship risk. But it does make one market truth harder to ignore: when tokenized dollars serve as core financial plumbing, compliance capability becomes part of the product itself.