Trad.Fi’s onchain credit plan brings equipment-finance workflows into the RWA buildout

Trad.Fi’s new pipeline is notable less for the headline dollar figure than for the type of credit it is trying to move onchain: operating loans tied to real equipment, real suppliers and real payment delays. That is the kind of private credit tokenization that tests whether RWA infrastructure can serve day-to-day commercial finance instead of staying concentrated in treasury funds and crypto-native lending loops.

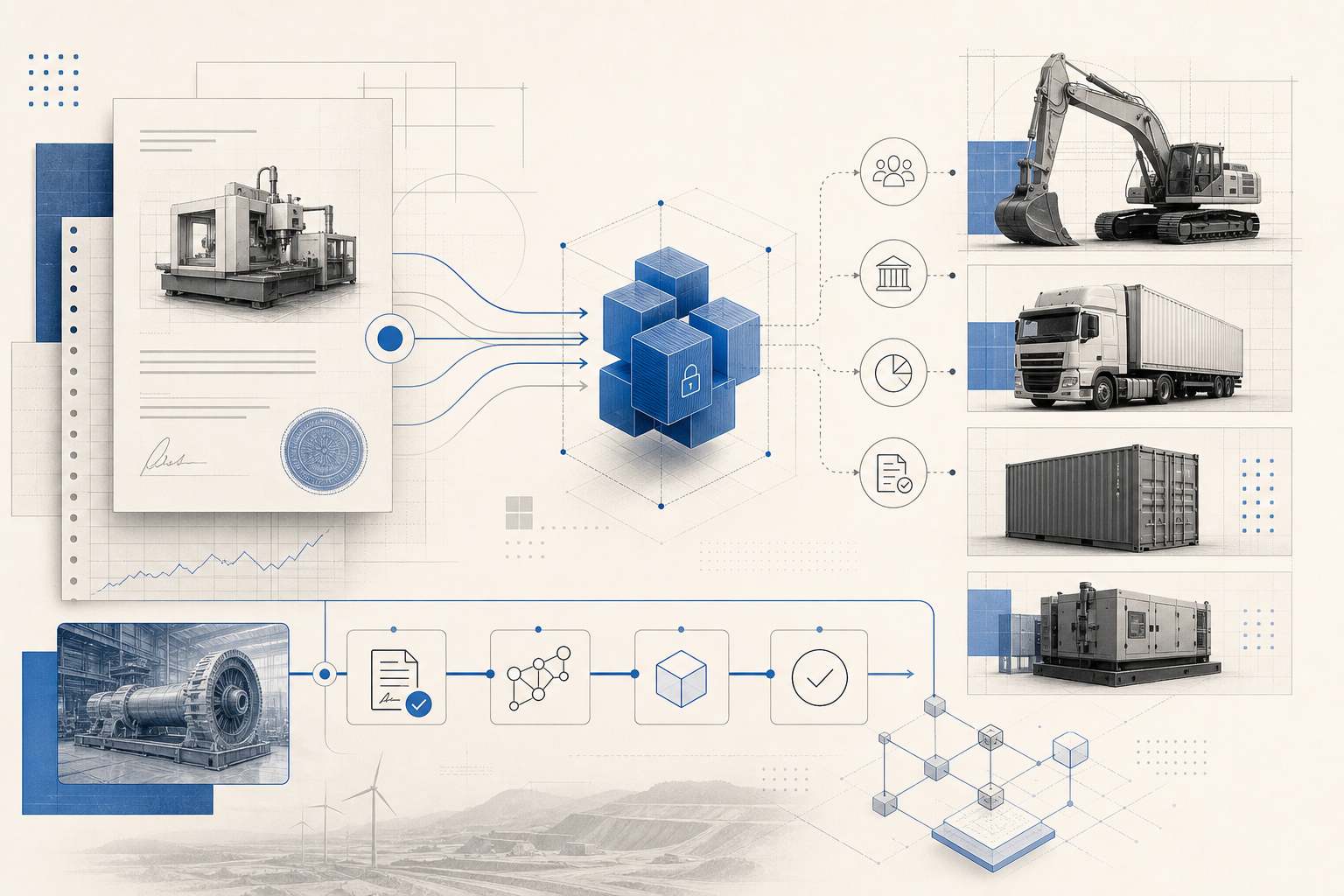

A planned push to bring up to $650 million of equipment-finance credit onchain is one of the clearer recent signs that RWA expansion is moving beyond treasury wrappers and into operating credit. Trad.Fi, a U.S. equipment-finance platform focused on small and mid-sized businesses, says it intends to place a four-year pipeline of private credit onto blockchain-based rails with treasury workflow support from W3. The immediate importance is not that a new number has been attached to the tokenization narrative. It is that the underlying loans are tied to a large, stubbornly paper-heavy corner of the real economy: financing for manufacturing equipment, industrial systems and residential solar installations.

That distinction matters. Much of the recent RWA growth has come from cash-equivalent products, tokenized government debt and institutional liquidity vehicles that are comparatively straightforward to map onto blockchain settlement. Equipment finance is different because it sits inside messy commercial workflows. Suppliers want payment before goods ship, customers often pay on delayed terms after installation, and distributors or contractors absorb the timing gap. Trad.Fi’s core pitch on its own site is that it can compress approvals dramatically, using digital underwriting and connected operating data to move from the traditional multi-week process toward same-day or single-business-day decisions. If that underwriting workflow can be paired with onchain capital records and funding rails, the result is closer to real-economy credit modernization than to a simple token wrapper.

The company’s public announcement adds the most specific details. Trad.Fi says the $650 million figure refers to a pipeline it expects to mint onchain over 48 months rather than capital already deployed, and describes that pipeline as backed by committed senior credit facilities and signed borrower intent. It also says an investor vehicle providing exposure to the underlying loans is expected to follow through a third-party operator. Those details are important because they narrow what is actually being launched. This is not a claim that hundreds of millions of dollars have already been originated onchain. It is a plan to tokenize a credit pipeline, formalize the records around it and later open a structured investment route into that flow.

W3’s role helps explain how the architecture is supposed to work. The press materials describe W3 as the programmable treasury layer that keeps capital productive until loans are ready to fund, then routes deployments through automated workflows while issuing an onchain record for each capital movement. W3’s own site presents the platform as infrastructure for autonomous finance, with private credit and digital yield among the use cases it is targeting. Put differently, Trad.Fi appears to be pairing loan origination and borrower acquisition with a separate system for treasury orchestration, capital tracking and verifiable execution. That is a sensible design choice for an RWA market that increasingly rewards specialized stacks instead of all-in-one monoliths.

The broader RWA implication is that tokenization is starting to be judged by whether it can improve working financial operations, not just create investable wrappers. Equipment finance is a useful test case because it is large, repetitive and operationally painful. If blockchain-based records can reduce funding friction, shorten approval cycles and give lenders a clearer capital trail, tokenization starts to look less like a distribution gimmick and more like upgraded market infrastructure. Trad.Fi’s own messaging emphasizes UCC-1 filings, collateral control and asset-backed lending discipline, which is exactly where serious RWA adoption has to live if it wants institutional durability.

There are still obvious execution questions. Onchain records do not eliminate underwriting risk, borrower defaults or documentation complexity. Legal agreements remain offchain, and the eventual investor vehicle has not yet launched or named its operator. The pipeline figure also needs to be separated from funded balances, because markets routinely confuse announced capacity with deployed assets. Even so, those caveats do not make the initiative unimportant. They simply clarify that the story is about operational buildout rather than instant scale.

On balance, the Trad.Fi program qualifies as a strong RWA signal because it links blockchain rails to an actual commercial credit function with visible inefficiencies and real collateral behind the loans. That is the kind of use case the sector needs more of. If tokenization is going to mature into mainstream capital-markets infrastructure, it has to show up in financing workflows that businesses already rely on, not only in products designed for crypto-native treasury management. Equipment finance is not the flashiest corner of the market, but it may be one of the more credible proving grounds for what onchain private credit can become.