Trace Finance’s $32 million round points to a more regulated model for stablecoin settlement in Brazil

Trace Finance’s Series A is more than a funding headline. It shows investor demand for bank-grade infrastructure that can connect local payment rails, FX handling and stablecoin settlement across Brazil and other emerging-market corridors.

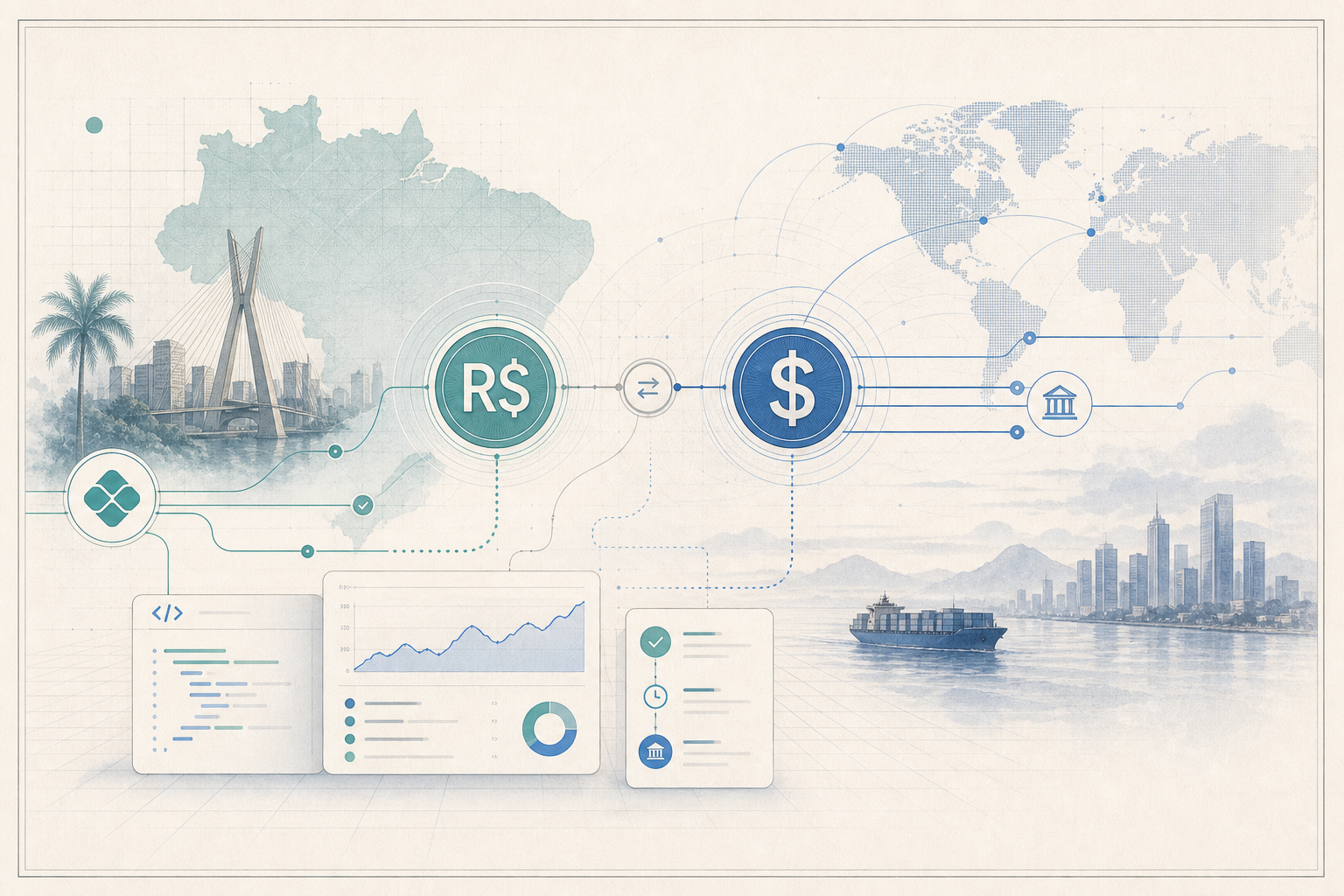

Trace Finance’s new $32 million Series A is a useful marker for where the stablecoin market is maturing. The headline is a venture round, but the more important signal is what investors are funding: regulated plumbing for cross-border money movement in a market where local bank access, foreign-exchange handling and compliance are still harder to scale than token settlement itself. In Brazil and the wider Latin American corridor, the commercial opportunity is not just issuing or holding digital dollars. It is building a licensed operating layer that lets enterprises convert, settle and reconcile those dollars against real payment rails without stitching together a patchwork of banks, brokers and crypto vendors.

The company said the round was led by CoinFund and included support from Coinbase Ventures, Haun Ventures, Jump Crypto, Paxos, Valor Capital, HOF Capital and other strategic backers. Trace said the capital will be used to expand its product footprint across Brazil, the United States, Asia-Pacific and other priority markets while deepening its capabilities in foreign exchange, bank connectivity, compliance and stablecoin settlement. The company also said it has processed more than $10 billion in cross-border volume to date, which, if sustained at enterprise quality, gives it a stronger operating case than many payment startups that still sell mostly on future network effects.

What makes the business relevant to RWA observers is the way it combines traditional payment infrastructure with stablecoin conversion rather than treating those functions as separate stacks. On its public product materials, Trace pitches named and virtual accounts in BRL, USD and EUR, 24/7 cross-border settlement through a single API, and BRL-to-USDC conversion in under a minute through Brazil’s Pix system. It also advertises payment connectivity across Pix, SPEI, ACH and SEPA. That mix matters because real-world asset activity does not stop at token issuance. Funds, brokers, exchanges and treasury teams still need reliable entry and exit points between local fiat systems and onchain dollar liquidity.

Brazil is a strategically important test case for that model. In the company’s financing materials, management describes the US-Brazil corridor as the proving ground for a broader emerging-markets strategy and points to regulation that treats virtual-asset cross-border flows as foreign-exchange activity. In practical terms, that pushes institutional volume toward providers that can operate with bank-grade controls instead of relying on informal crypto routing alone. Trace’s own website leans heavily into that posture, highlighting AML and CFT alignment, automated KYC, transaction monitoring and audit trails as part of the core product rather than as an add-on for enterprise sales decks.

There is also evidence that the company is trying to become network infrastructure instead of just a direct service provider. In April, Borderless.xyz announced Trace as a partner for Brazil corridors, saying the integration would give participants access to BRL on- and off-ramps, named accounts and third-party payments while reducing the cost of stablecoin-based foreign exchange. Borderless described its own network as covering more than 50 countries and 23 currencies. For Trace, that kind of integration is strategically important: the value of regulated local settlement rises when it can be embedded inside other payment and treasury workflows rather than sold one client at a time.

The broader RWA implication is that stablecoin adoption in enterprise finance is becoming less about the token and more about the settlement environment around it. A corporate treasury team or payments platform may care about USDC liquidity, but it also cares about whether BRL conversion is available on weekends, whether counterparties can be screened properly, whether local disbursements arrive on domestic rails, and whether an auditor can trace the flow from wallet to bank account. Those are the operational details that determine whether tokenized cash becomes part of everyday finance or remains a specialist tool used only in narrow corridors.

If Trace executes, its round will matter less as another fintech funding announcement and more as proof that emerging-market stablecoin infrastructure is consolidating around regulated access points. That is a meaningful development for RWA markets because the next stage of tokenized finance will depend on ordinary settlement reliability as much as on-chain composability. The firms that win will not necessarily be the loudest issuers or the most visible blockchains. They will be the ones that make local money systems and global digital-dollar liquidity work together without creating new operational friction.