Stablecoin rails are giving micropayments another real-world test in machine commerce

Stablecoin settlement is reviving an old internet payments idea, but the new demand signal is coming less from human readers and more from software, APIs and autonomous agents. Open payment standards and always-on dollar tokens are reducing the transaction-cost floor that made sub-dollar commerce hard to scale on legacy rails.

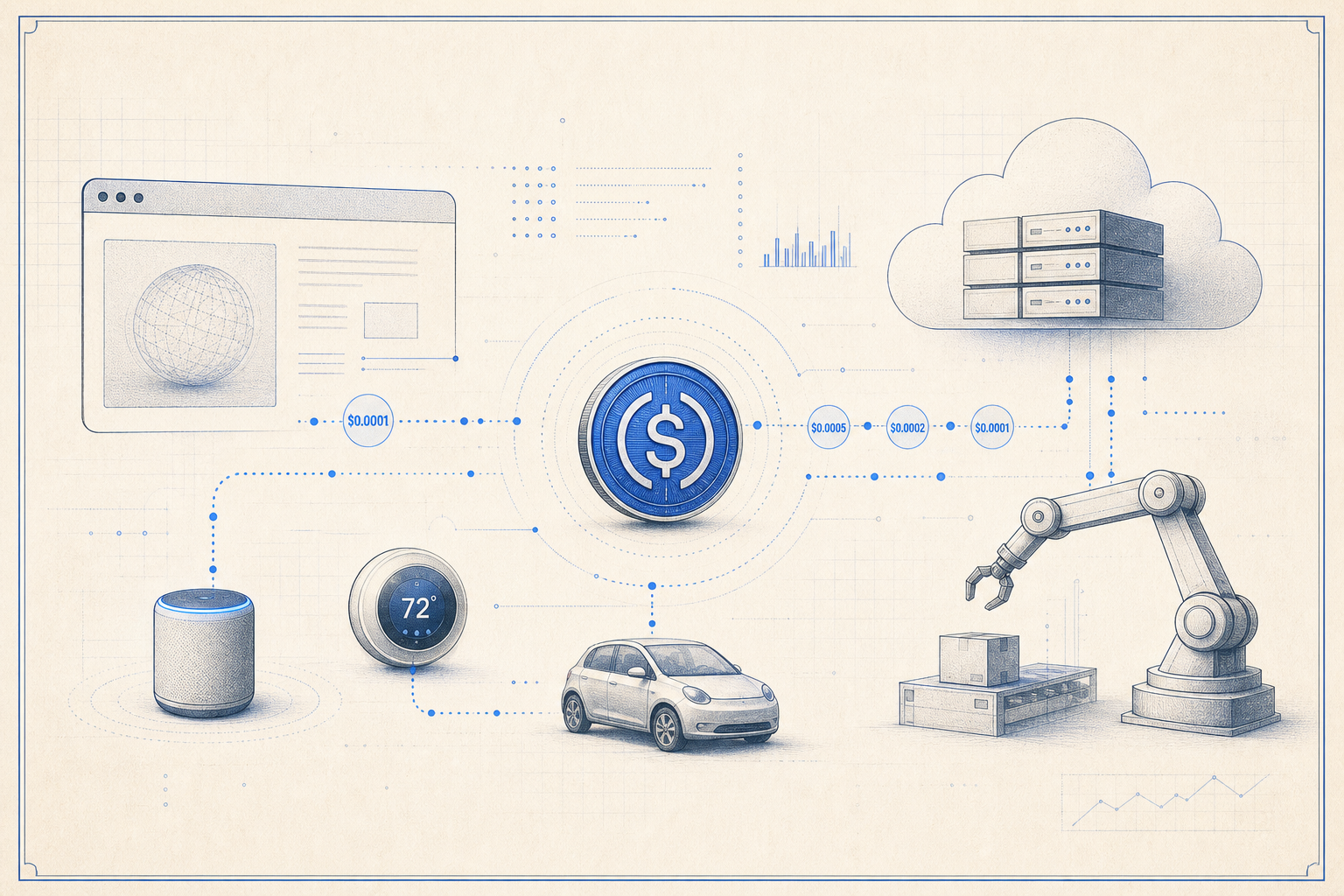

Micropayments have been a recurring promise of the internet era, but the concept usually stalled on one practical issue: the rails were too expensive, too slow or too operationally heavy for transactions worth pennies. A fresh wave of industry attention this week has put the topic back on the agenda, with stablecoins increasingly framed as the settlement layer that can make very small digital payments economically viable. The shift matters for RWA markets because it shows dollar-backed tokens moving beyond trading and treasury management into everyday transaction design.

The technical case is stronger than it was in earlier payment cycles. Stablecoin transfers can be executed around the clock, settled without card-network interchange, and embedded directly into software flows rather than bolted on after the fact. That changes the minimum practical ticket size for certain transactions. When the payment instrument is already digital cash onchain, the economics of charging for a single API call, a short burst of compute, a research query or a narrow piece of premium content look materially different from the economics of charging the same amounts over conventional card rails.

One reason the conversation is gaining traction now is the emergence of machine-native payment tooling. Coinbase-backed x402 documentation describes the protocol as an open standard for internet-native payments, built so applications can attach payment requirements directly to HTTP requests. In plain terms, that means software can ask for payment at the same layer where it asks for access, without forcing the user through a separate checkout experience. That architecture is particularly relevant for autonomous agents and API-based services, where the buyer may be another piece of software rather than a human deciding whether to enter card details for a ten-cent transaction.

Stablecoin issuer materials point to the same operational advantage from the asset side. Circle’s developer documentation presents USDC as a fully reserved digital dollar that is redeemable one-to-one for U.S. dollars and available on public blockchain networks with 24/7 transfer capability and low-cost settlement. Those characteristics do not guarantee micropayment adoption on their own, but they remove a major historical constraint. Earlier micropayment models often failed before the business model could even be tested because fee structures consumed too much of the transaction value. With stablecoins, the cost problem is no longer as decisive as it was when card processing defined the default path for digital commerce.

That does not mean the commercial problem has been solved. Consumers have repeatedly shown that they prefer subscriptions, bundles and ad-supported access over constantly evaluating tiny purchases. The stronger near-term use case may therefore be software commerce rather than consumer media. Agents paying for authenticated data, bots purchasing short-lived API access, enterprise systems settling usage-based services, or devices paying one another for bandwidth and compute are all more plausible than a broad return to pay-per-article web browsing. In those contexts, the convenience cost of making a payment decision is near zero because the decision can be automated.

For RWA observers, this matters because it expands the utility story for tokenized dollars at a time when the sector is trying to prove that onchain finance can support real transaction volume outside speculative markets. The most durable RWA products tend to win when they improve operational throughput, auditability or capital efficiency for existing financial behavior. Micropayments fit that pattern if stablecoins become the mechanism for metered access, machine-to-machine settlement and fine-grained digital invoicing. The opportunity is less about resurrecting an old dream unchanged and more about identifying transaction types that were uneconomic until programmable dollars and programmable access controls arrived together.

The next milestone to watch is not whether companies can demonstrate a micropayment in a lab setting. That has been possible for years. The real test is whether developers and payment operators can turn these flows into repeatable products with clear pricing, risk controls, refund logic, compliance handling and enough user benefit to change behavior. Stablecoins have lowered the infrastructure barrier substantially. The remaining question is whether businesses can pair that infrastructure with distribution and product design strong enough to make tiny digital payments routine rather than merely possible.