South Korea links national-asset reform to tokenized bond infrastructure

South Korea’s latest economic roadmap does more than acknowledge digital assets as a policy category. It ties public-sector crypto management, legal asset reform and a 2027 tokenized bond pilot into one evolving state-finance agenda.

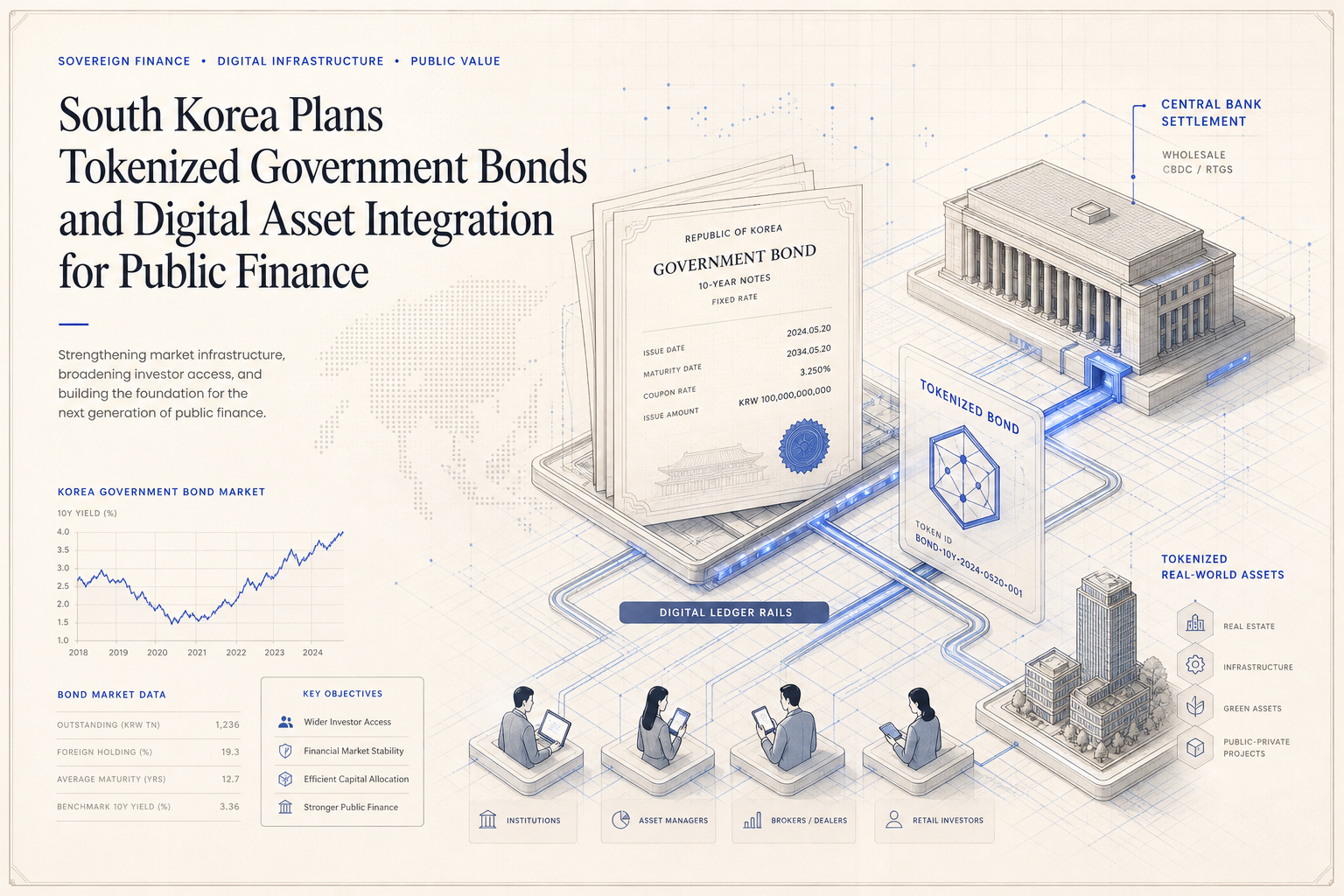

South Korea’s latest economic policy roadmap points to a more structural approach to tokenization than many government announcements that treat blockchain as a narrow pilot topic. The plan described by the finance ministry would revise the country’s long-standing national property framework so that virtual assets and intellectual property can be recognized within the definition of national assets, while also reaffirming a 2027 pilot for tokenized government bonds. Taken together, those measures suggest Seoul is not only testing tokenized instruments at the market edge. It is beginning to adapt the legal and administrative machinery of the state to a world in which digital assets may sit alongside conventional public-sector holdings.

The importance of that framing is easy to miss. Governments regularly talk about blockchain experimentation, but those programs often remain boxed into innovation sandboxes with little connection to budget management, sovereign funding or public balance-sheet operations. South Korea’s roadmap is more integrated. It pairs an update to national asset governance with work on tokenized debt, and it does so after months of official messaging about institutionalizing digital assets inside economic policy rather than treating them solely as a consumer-protection problem. Earlier ministry materials for the 2026 Economic Growth Strategy explicitly called for digital assets to be institutionalized and utilized, indicating that this week’s roadmap is part of a longer policy sequence rather than a standalone headline.

That sequence also includes more operational groundwork. In April, the finance ministry outlined a public-sector management framework for virtual asset holdings across the central government, public institutions and local governments. The plan called for designated personnel, custody and compliance guidelines, and measures to prepare for a future in which public entities may hold more digital assets and need those holdings to be managed systematically within the national property framework. The new roadmap effectively extends that logic from internal controls toward market structure, connecting the question of what the state can hold with the question of how the state might issue or administer tokenized financial instruments.

The bond pilot is the clearest RWA signal in the package. According to the roadmap, South Korea intends to begin a tokenized government bond pilot in 2027 and explore connections to the Bank of Korea’s digital-currency infrastructure. Officials are also studying interoperability between the central bank’s blockchain environment and other distributed-ledger systems. If that architecture is carried through, the pilot would not just test whether a sovereign instrument can be represented as a token. It would test whether issuance, ownership records and settlement can be coordinated across public infrastructure in a way that reduces transfer friction and modernizes the handling of government securities.

Another notable element is the ministry’s stated interest in tokenizing state-owned real estate so that retail investors could participate and share in returns. That idea remains exploratory, and many details are still missing, including how assets would be selected, what investor protections would apply and whether such offerings would be structured through funds, trusts or direct fractional interests. Even so, the concept matters because it broadens the state’s tokenization agenda beyond sovereign debt. It suggests officials are studying tokenization as a tool for mobilizing access to public assets, not only as a settlement upgrade for bond markets.

The legal timetable is also worth watching. The roadmap points to amendments due in February 2027 that would treat approved blockchain record systems as legally recognized books of record for securities ownership and transfer within Korea’s capital-markets framework. That kind of legal recognition is often the difference between an attention-grabbing pilot and a durable financial-market change. Tokenization cannot scale simply because distributed ledgers exist; it scales when the legal system recognizes digital records as authoritative for ownership, servicing and transfer. South Korea appears to be working toward that recognition in parallel with its product pilots rather than leaving the law to catch up later.

None of this means the country has solved tokenized finance. Execution risk remains high, especially where sovereign issuance, retail participation and central-bank-linked infrastructure intersect. But the policy direction is more coherent than the typical test-and-learn announcement. South Korea is steadily building a chain from economic strategy, to public-sector asset management, to legal reform, to sovereign-market experimentation. For the broader RWA sector, that makes the country worth watching not because it has the largest tokenized market today, but because it is trying to align state finance, market law and digital infrastructure early enough for tokenization to become a governable part of the financial system rather than a permanent pilot.