SBI turns JPYSC into a yield product, extending Japan’s stablecoin rollout beyond payments

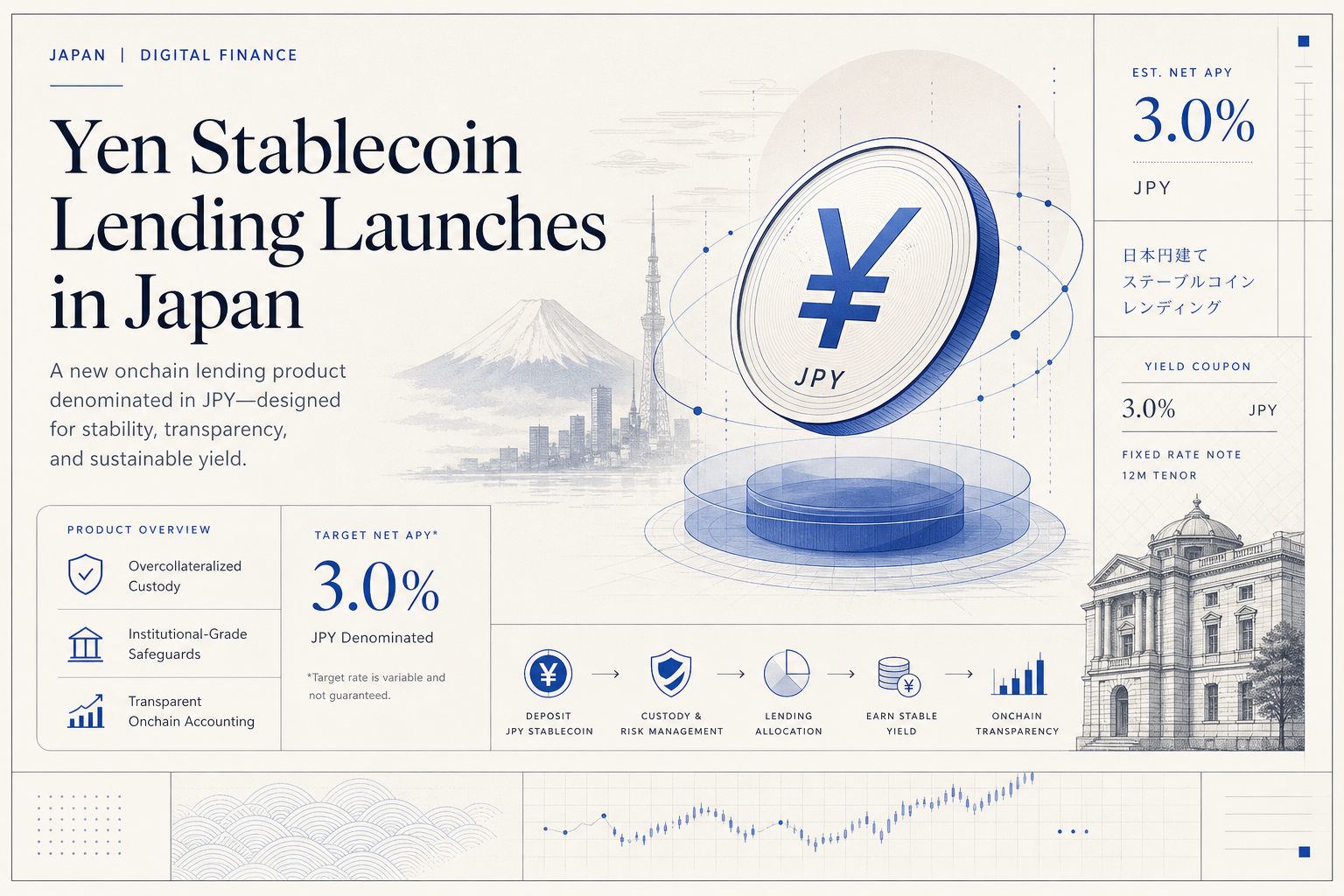

SBI VC Trade is opening Japan’s first trust-structured yen stablecoin lending product, offering an initial 3% annualized rate on 12-week JPYSC loans. The launch matters less as a retail promotion than as evidence that regulated stablecoins in Japan are starting to move from pure transfer rails into balance-sheet and treasury use cases.

Japan’s regulated stablecoin market has spent much of the last year proving that tokenized money can be issued, distributed and redeemed inside a tightly supervised domestic framework. SBI VC Trade’s new JPYSC lending program adds a more consequential next step: turning a yen-backed stablecoin from a payments instrument into a product that can sit on a balance sheet and earn a return. According to an official notice published by SBI VC Trade on July 13, applications for the new service will open on July 16, allowing customers to lend the trust-structured yen stablecoin JPYSC to the platform for a 12-week term at an initial annualized rate of 3%. That framing may sound retail on the surface, but the deeper signal for RWA markets is that Japan is beginning to test what regulated onchain cash can do once it is treated as usable financial inventory rather than only a settlement token.

The structure described by SBI makes clear that this is not being positioned as a bank-deposit substitute in the legal sense. The company says JPYSC lenders will transfer the token to SBI VC Trade under a consumption-loan arrangement, receive the same token back at maturity with an added lending fee, and accept that the position is not covered by deposit insurance and generally cannot be cancelled early. The release also states that assets lent through the program fall outside statutory segregation rules that would otherwise apply to customer electronic payment instruments, meaning users are taking direct platform credit risk. That risk disclosure is important. It shows Japan’s stablecoin market is not simply importing the language of savings products into a token wrapper; it is testing how regulated digital cash can support yield-bearing services while still preserving the legal distinctions between deposits, custody arrangements and lending exposures.

In practical terms, the commercial pitch is straightforward. SBI says the launch rate of 3% annualized for a 12-week term sits above the range it cited for ordinary yen time deposits, and that normal issuance rounds are expected to price between 1% and 3% depending on market conditions. The company also emphasizes that the service returns proceeds in JPYSC rather than in fiat, reinforcing that the product is designed to deepen circulation of the stablecoin itself. That is strategically different from simply offering a promotional yield to acquire users. If JPYSC becomes a token that investors are willing to hold for transactional liquidity, then lend for short-duration return, and later reuse in other onchain workflows, it begins to look less like a one-off fintech product and more like the cash leg needed for a broader tokenized-finance stack.

That broader stack is already visible in the surrounding SBI strategy. On the same day as the lending launch, SBI Holdings announced a strategic partnership with the Solana Foundation aimed at building an onchain financial market originating in Japan, according to the company’s official release metadata and title. Cointelegraph’s reporting on the lending program also notes that the initiative tied into the group’s wider push to expand infrastructure for stablecoins, tokenized assets and cross-border settlement. Even without all operational details yet public, the alignment is notable: one arm of the group is distributing a yield-bearing yen stablecoin product to users, while the parent is signaling that the next phase involves larger-scale market infrastructure rather than isolated token pilots. For RWA operators, that combination matters because cash instruments only become systemically useful when issuance, settlement, distribution and secondary workflows are being built together.

Japan’s regulatory posture gives this development extra weight. SBI VC Trade says it is the only domestic operator currently licensed to offer stablecoin distribution and trading services to retail users under the electronic payment instruments framework, and it already supports USDC alongside JPYSC and RLUSD. Earlier this year the firm introduced a USDC lending service, and the new JPYSC program extends the same logic into local-currency stablecoins. That progression is easy to miss, but it is one of the clearest markers that Japan’s market is moving from experimental access toward product layering. In other words, regulated stablecoins are no longer being judged only on whether they can be listed or transferred; they are being evaluated on whether they can support treasury-style functions, idle-balance monetization and ultimately collateral-aware market activity.

The relevance to RWA infrastructure is especially strong because tokenized securities markets need reliable onchain cash tools in order to become operationally efficient. Settlement assets that can move on regulated rails, remain denominated in domestic currency and be reused across payment, trading and financing workflows are a prerequisite for deeper tokenization in bonds, funds and other real-world assets. Japan has already seen steady progress in tokenized securities issuance, and the industry’s next bottleneck is less about whether assets can be represented onchain than whether the surrounding money layer can support real financial behavior. A yen stablecoin that can be held, lent and potentially integrated into broader market plumbing is a meaningful answer to that problem, even if today’s product is still small and tightly bounded.

None of this means the market has solved the trust and risk questions. The SBI release is explicit that users face issuer and platform exposure, cannot rely on deposit insurance and may lose access to tokens if the intermediary fails. Those limitations should temper any narrative that tokenized cash products are automatically superior to bank balances. But they do not diminish the importance of the step. What SBI has put into market is a regulated experiment in making domestic stablecoins economically useful beyond transfer. If Japan continues down that path, the country may end up showing not just how to authorize stablecoins, but how to fit them into the funding, collateral and settlement mechanics that a mature RWA ecosystem actually needs.