Pyth’s 24/7 index launch targets a missing layer in tokenized stock and commodity markets

Pyth’s new continuous indexes are aimed at one of tokenization’s hardest operating problems: how to keep reliable reference pricing alive when the underlying stock or commodity market is closed. If tokenized equities and commodity products are going to trade around the clock, pricing infrastructure has to become an always-on market utility rather than a market-hours afterthought.

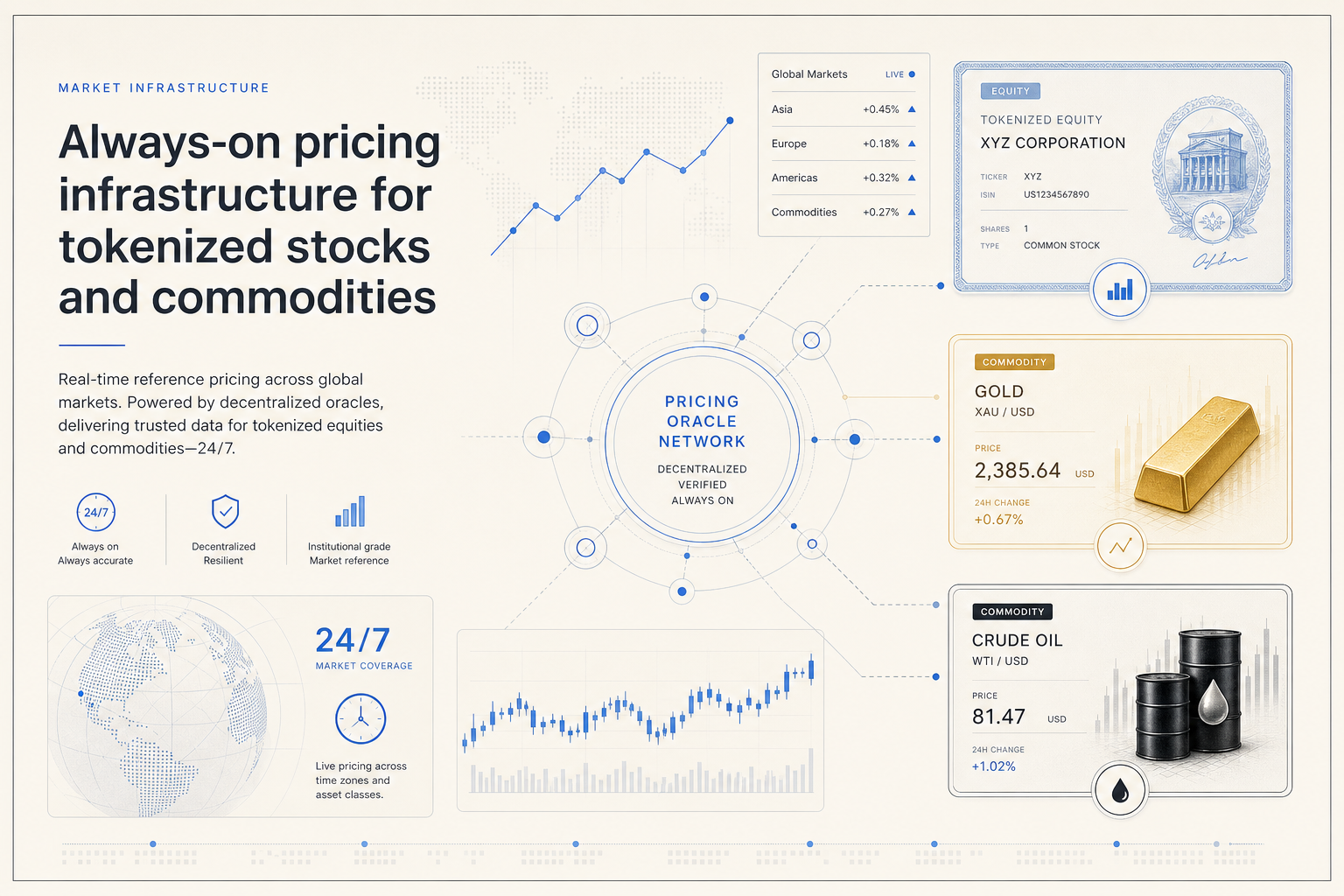

The newest bottleneck in tokenized markets is no longer simply issuance. It is market structure. Pyth Network’s launch of continuously updated indexes for U.S. stocks, metals and oil is notable because it goes after a piece of infrastructure that tokenized-equity and commodity products increasingly need but still do not fully control: a reference price that remains usable when the primary exchange is closed. As more venues list tokenized stocks, commodity-linked instruments and perpetual products tied to real-world assets, the market has moved ahead of the pricing conventions that traditional finance built around fixed trading sessions.

The source reporting says Coinbase, Kraken, dYdX and Nado are already adopting the new indexes, which Pyth positions as inputs for perpetual futures, tokenized assets, prediction markets, derivatives settlement and benchmark construction. That matters because it suggests this is not a speculative concept launch with no downstream users. It is being introduced as a service layer for venues that want to keep products live outside New York cash equity hours or commodity pit hours. In practical terms, that means the value proposition is less about a new ticker and more about keeping market plumbing intact across nights, weekends and cross-border trading windows.

Pyth’s own launch materials make the scope clearer. The network says the first wave covers single-name U.S. equity indexes for names such as Nvidia, Tesla, Apple, Microsoft, Google, Intel, Robinhood, Strategy and Circle, along with gold, silver, WTI and Brent. It also says it worked with MarketVector, the VanEck-owned index provider, on thematic baskets tied to artificial intelligence, defense, China and technology. That combination is revealing. Pyth is not only trying to mirror isolated assets; it is assembling the reference layer needed for an entire class of tokenized and derivatives products that look more like capital-markets packages than one-off crypto wrappers.

The underlying reason this matters to RWA markets is simple: tokenization breaks the old assumption that market access and market hours are the same thing. A tokenized Apple instrument can be transferred, margined or referenced by an onchain system whenever the blockchain is operating, but the underlying U.S. equity market still closes. That gap creates valuation, liquidation and risk-management problems unless a venue has a defensible methodology for producing continuous prices. Pyth describes these indexes as proprietary 24/7 products built from its price feeds, and its developer documentation reinforces the broader claim that its stack is designed for institutional and DeFi use cases with sub-second updates, wide blockchain coverage and first-party data contributors. Whether one prefers Pyth’s methodology or not, the product is clearly aimed at solving an operational problem the tokenization sector can no longer ignore.

There is also a competitive angle. Exchanges and issuers that want to offer around-the-clock exposure to equities, commodities or thematic baskets need a trusted data layer that can survive periods when the cash market is dark. If that layer is weak, products will face wider spreads, harder-to-defend liquidations and more skepticism from institutions evaluating whether tokenized exposures can be run with credible controls. If the layer is strong, the economics of 24/7 distribution improve. That is why an index launch can matter even before it directly increases trading volume: it expands the set of financial products that can plausibly be offered onchain without depending on market-hours shortcuts.

The launch also says something broader about where RWA infrastructure is heading. For the past year, the tokenization conversation has been dominated by issuance growth in treasuries, funds and private credit. Public equities and commodity-linked products have advanced more unevenly because they need stronger trading, custody and price-reference systems than simple buy-and-hold wrappers. Continuous indexes are part of that missing stack. They do not solve the legal or regulatory questions around tokenized securities, but they do address the practical market-data problem that emerges the moment a venue tries to make these products trade globally and continuously.

That makes Pyth’s move worth watching even beyond its own network economics. The test is not whether an oracle provider can say tokenized markets are 24/7; the test is whether exchanges, market makers and structured-product issuers can operate as if that statement is true. A pricing layer that covers names like Apple and Circle alongside gold and crude is a step toward that outcome. If adoption sticks, the significance will be less about one company winning an oracle headline and more about tokenized real-world assets acquiring another piece of durable capital-markets infrastructure.