Payward targets the enterprise card and treasury layer of stablecoin adoption with planned Reap deal

Payward's planned acquisition of Reap points to a more practical stablecoin battleground: corporate cards, cross-border payouts and treasury operations rather than retail crypto features. The deal stands out because it links tokenized-asset infrastructure to the real payment workflows enterprises already run.

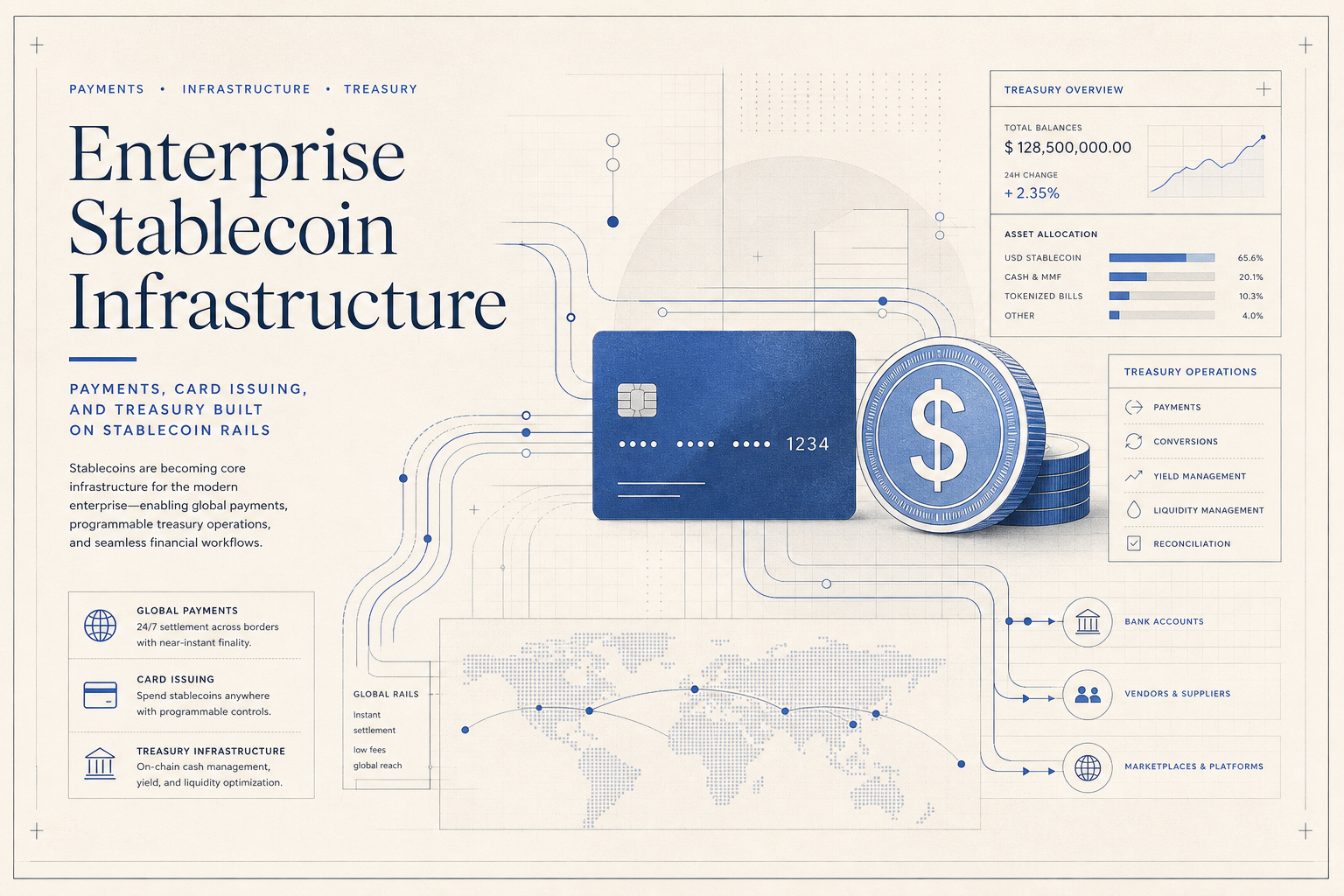

Payward’s agreement to acquire Hong Kong-based Reap is a useful signal about where stablecoin infrastructure is becoming commercially meaningful. The deal is not centered on retail trading or another exchange feature. It is aimed at the operating layer behind business payments: corporate cards, cross-border payouts, treasury movement and the settlement plumbing that sits between card networks, banking rails and digital assets. That is a more durable part of the stablecoin thesis than headline-grabbing consumer experiments, because it addresses workflows companies already run every day.

The underlying transaction also looks narrower and more concrete than some early reports suggested. Reap’s co-founders said the company has entered into an agreement to be acquired by Payward, the parent platform behind Kraken and other regulated financial products, with closing still subject to customary regulatory approvals expected in the second half of 2026. That matters because the strategic message is not that a merger has already been fully integrated. It is that Payward wants to add a stablecoin-native payments stack that Reap spent years building in Asia, especially around card issuing and cross-border business transfers.

Reap’s own product materials show why that stack is attractive. Its payments flow lets businesses fund outbound transfers with USDC or USDT and deliver fiat to recipients across local rails and SWIFT channels, with support for more than 18 settlement currencies and coverage across more than 220 countries and territories. On the card side, Reap markets Visa corporate cards that can be repaid in either stablecoins or fiat, with controls for budgets, merchant restrictions and distributed team spending. In practical terms, that means stablecoins are not being pitched as a consumer lifestyle brand. They are being inserted into familiar enterprise surfaces such as accounts payable, employee spend and treasury allocation.

That is the part of the story RWA builders should pay attention to. Tokenized assets need usable cash legs, and businesses that hold capital onchain still need to pay suppliers, fund operations and manage reconciliation without dropping back into slow manual banking processes each time money moves. Reap itself made that point this week in a separate note on tokenized stocks, arguing that onchain equities only achieve their full efficiency when the settlement asset is also native to the chain. A stablecoin-funded payment and card layer does not solve tokenization on its own, but it does address one of the most persistent operational gaps between tokenized assets and real corporate finance workflows.

Payward brings the part of the stack Reap could not easily build alone. In the founders’ note, Reap said the next stage required broader regulatory coverage across the United States, Europe and new payment corridors, plus deeper liquidity, custody and partner distribution. The company described Payward as already operating across crypto trading, custody, tokenized assets, on- and off-ramps, derivatives and a large B2B partner base. If that integration is executed well, the combined platform could offer treasury movement, payment initiation, card issuance and digital-asset settlement inside one institutional workflow instead of forcing enterprises to stitch together separate exchanges, issuers, banks and middleware vendors.

The commercial opportunity is obvious, but so are the constraints. Stablecoin infrastructure only becomes core enterprise plumbing if finance teams trust the controls as much as the speed. That means licensing, sanctions screening, redemption certainty, ledger visibility, auditability and clean ERP handoffs matter just as much as transaction throughput. Reap’s current positioning acknowledges that reality: its pitch is full of compliance language, local rails, spend controls and treasury tooling rather than crypto-native ideology. That is typically a healthier sign for adoption than promises of instant disruption, because the real buyers in this market are controllers, treasury teams and CFOs.

For RWA Trails, the broader implication is that stablecoins are increasingly being built as operational money for tokenized markets, not just as exchange collateral. When card programs, supplier payments and treasury balances can all be funded from the same onchain dollar base, the distance between tokenized assets and ordinary business finance gets shorter. Payward’s planned Reap acquisition will need to clear approvals before any of that thesis is proven at scale, but the direction of travel is clear: the next contest in stablecoin infrastructure is moving deeper into institutional payments, where the winners will be the firms that combine regulatory credibility with usable day-to-day financial workflows.