Mastercard’s new machine-payments stack brings stablecoin settlement into AI commerce

Mastercard’s Agent Pay for Machines is more than another AI pilot: it is an attempt to make stablecoin-capable, policy-controlled payments usable by software agents operating at machine speed. The launch matters because it pushes tokenized cash and multi-rail settlement closer to real enterprise workflows instead of keeping them inside crypto-native demos.

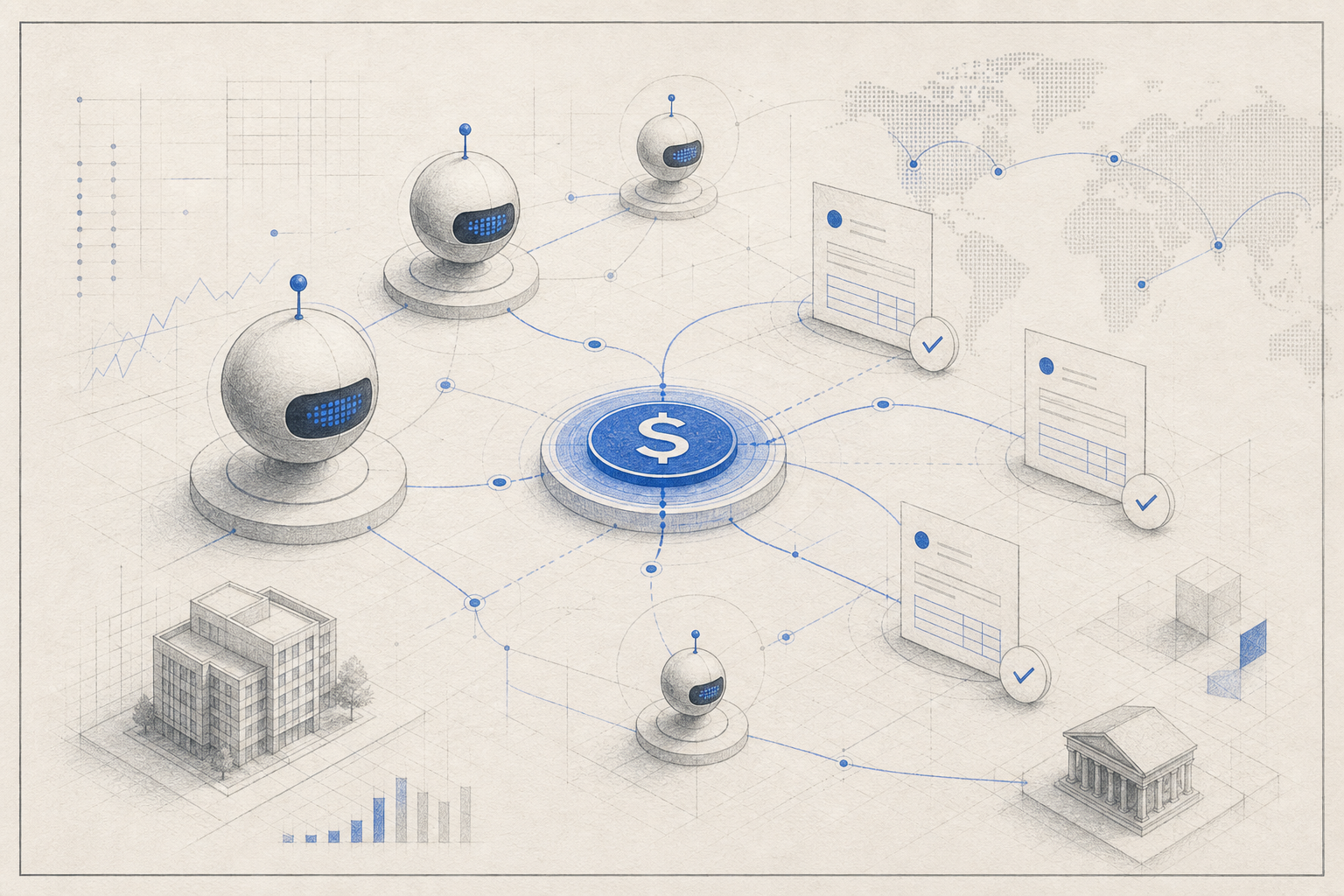

Mastercard is making a direct play for one of the next operational layers of digital finance: payments initiated by software rather than by people. Its new Agent Pay for Machines program is designed to let verified AI agents discover service providers, spend against pre-approved limits and settle transactions across multiple rails, including stablecoins. That matters for RWA markets because tokenized cash has long needed a stronger real-economy demand story. If machines begin paying for hosting, data, APIs, logistics or other digital and physical services on a continuous basis, the market will need settlement instruments that are programmable, always available and easier to route across different networks than conventional banking rails.

The launch is not framed as a crypto-native experiment. It is being positioned as enterprise payment infrastructure with identity, authorization and settlement controls built in. Reporting around the rollout indicates the service supports payments across cards, bank-connected methods and stablecoins while keeping Mastercard’s trust and acceptance network in the loop. In practical terms, the company is trying to answer a simple question before agentic commerce scales: how does a business allow software to buy things on its behalf without turning every automated action into an uncontrolled payments risk? Mastercard’s answer is to define permissions upfront and make settlement policy part of the product design rather than an afterthought.

That architecture becomes clearer in Mastercard’s own product materials. The workflow starts with an agent assembling a plan and estimated budget, after which the business approves a spending limit using a chosen funding source such as cards, a stablecoin wallet or a credit facility. Mastercard says that authorization can be recorded in an onchain smart contract. The agent then executes micro- and macro-payments using verifiable offchain credentials, while service providers aggregate transactions and receive payout in their preferred currency, whether fiat or stablecoin. That combination of bounded authority, machine-speed execution and optional tokenized settlement is the important feature here. It shows Mastercard is not just experimenting with AI interfaces; it is trying to package control logic and programmable money into a production-style payments flow.

The stablecoin angle is especially relevant because autonomous systems do not fit neatly into the operating hours and reconciliation habits of legacy finance. If software agents are expected to transact continuously, enterprises will want payment methods that support faster movement of value, clear audit trails and more flexible payout options across jurisdictions and platforms. Stablecoins are not the only answer, but they are one of the few payment instruments built for 24/7 transfer, deterministic denomination and API-native settlement. Mastercard’s design suggests it sees tokenized dollars as a complementary rail inside a broader payments stack, not as a wholesale replacement for cards or bank transfers. That is a more plausible near-term commercial model than the idea that enterprises will suddenly move all agent payments fully onchain.

The partner set also gives the rollout more weight than a typical concept announcement. Mastercard says 32 initial participants and supporters are involved, spanning crypto infrastructure, payment processors and enterprise tooling. The list includes Coinbase, Stripe, Adyen, Anchorage Digital, Ripple, Polygon, Solana Foundation, OKX and several agent-focused software companies. That breadth matters because machine commerce will fail if identity, walleting, payments acceptance, settlement guarantees and developer tooling remain fragmented across separate stacks. A network-level coordinator with both card-era distribution and blockchain relationships has a better chance than most firms at getting counterparties onto shared rules, even if the commercial model still needs to be proven in live volume.

For RWA observers, the broader signal is that tokenized cash is gradually moving from treasury-product adjacency into transaction infrastructure. Much of the recent onchain asset growth has centered on tokenized funds, Treasury wrappers and pre-IPO market access, where the settlement asset is important but often secondary to the investment product itself. Mastercard’s push highlights a different demand vector: software-driven commercial activity that may require programmable dollar liquidity as part of the workflow. If that category grows, stablecoins could become less dependent on crypto trading demand and more embedded in enterprise operating systems, procurement flows and machine-to-machine service payments.

There are still material questions. Enterprises will need clarity on liability, fraud recovery, dispute handling and the legal status of agent instructions. Developers will need better abstractions for spend policies, credential revocation and cross-rail reconciliation. Regulators will also care about how stablecoin settlement, data sharing and delegated payment authority are governed when the actor initiating the purchase is not a human user clicking through a checkout screen. None of that is solved by a launch announcement. But the design choices already disclosed point to where the market is heading: AI commerce will need governed payment permissions first, and only then will tokenized cash rails have a real chance to scale inside it.

The result is a story bigger than a single product release. Mastercard is effectively testing whether agentic commerce can be turned into a regulated, auditable payments category instead of a loose collection of demos. If it works, stablecoins gain a credible path into mainstream commercial settlement flows through a familiar enterprise channel. If it stalls, that will say something equally important about the friction still facing tokenized money outside trading and treasury use cases. Either way, this is one of the clearer signs that the next stablecoin battle may be fought less around consumer wallets and more around the software systems that increasingly act on behalf of businesses.