South Korea’s Project Hangang pushes tokenized deposits toward production — with privacy now the critical design question

South Korea’s Project Hangang is turning tokenized deposits into a live market-structure test, but the latest Bank of Korea paper leaves one of the hardest questions underexplained: how privacy works inside a unified ledger for banks, users and central-bank settlement.

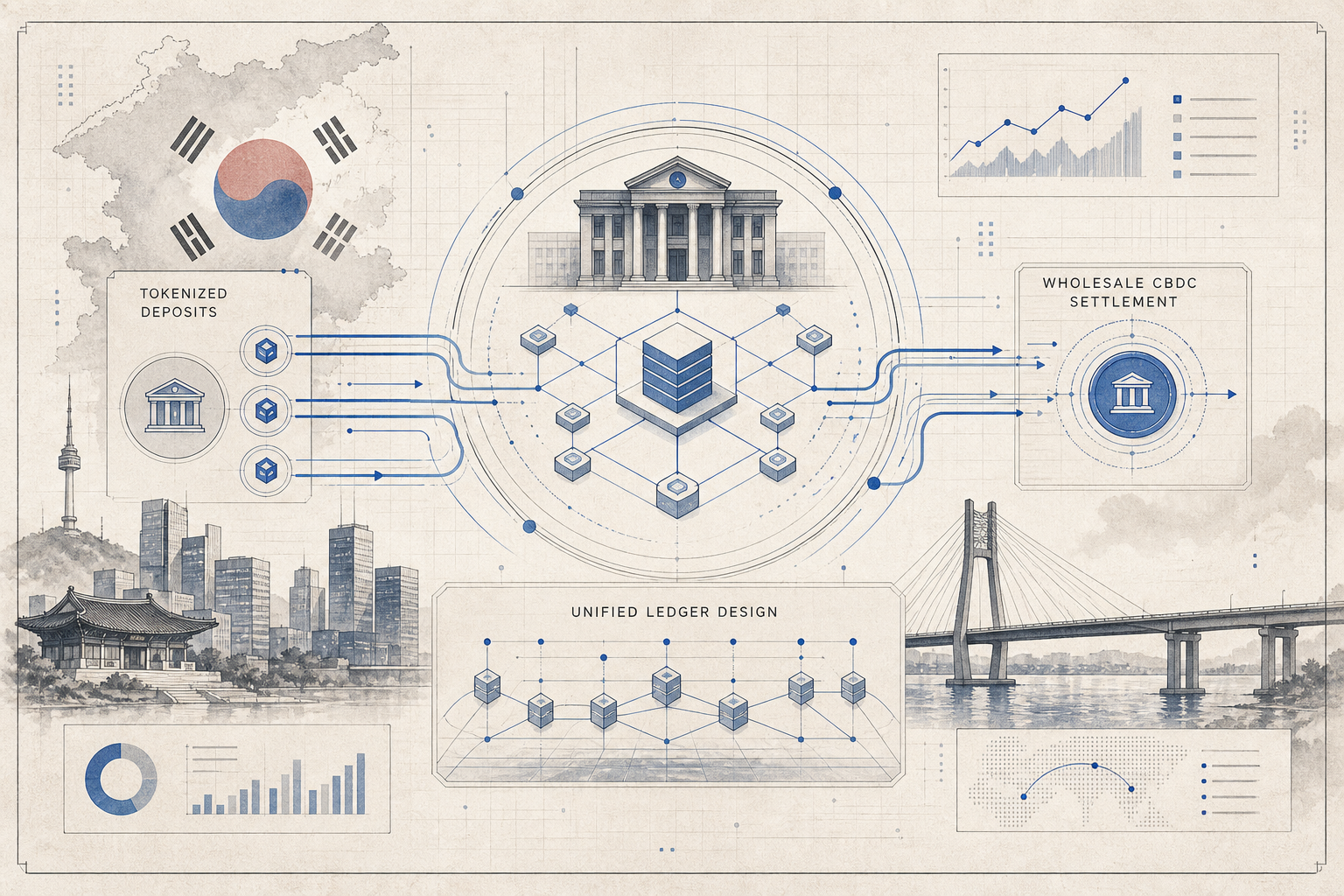

South Korea’s latest work on tokenized money is becoming more consequential — and more policy-sensitive — at the same time. In a new discussion paper released ahead of the ECB Forum, the Bank of Korea again framed Project Hangang as a blueprint for a future monetary system built around commercial-bank tokenized deposits and wholesale central bank money. The architecture is notable on its own. What makes the latest document more important is what it leaves unresolved: how privacy should work when retail-facing payments, bank-issued tokenized money and central-bank settlement all sit inside one coordinated ledger environment.

At the core of the design is a familiar but strategically important split of responsibilities. The Bank of Korea would issue wholesale CBDC for interbank transfers and final settlement, while commercial banks would issue tokenized deposits to end users inside the same network. That approach is meant to preserve the two-tier monetary structure rather than replace it with direct retail central bank accounts. In practice, it positions tokenized deposits as the consumer-facing payment instrument and reserves the central bank layer for settlement finality, supervision and system integrity.

This is not a conceptual exercise anymore. In the project’s first live testing cycle, the Bank of Korea and participating banks opened roughly 81,000 wallets and processed more than 114,000 transactions, according to the project’s March phase-two update. The initial bank cohort is now expanding from seven institutions to nine. Earlier Bank of Korea and joint-agency materials also made clear that the initiative is designed as a public-private market infrastructure project, with the Financial Services Commission, the Financial Supervisory Service and the BIS involved around policy coordination or technical advice.

What stands out in the latest paper is the tension between the sophistication of the system design and the relative silence around privacy in the current public framing. That matters because a unified ledger for tokenized deposits is not just another payment rail. It can concentrate operational visibility across wallet issuance, transaction validation, programmability and settlement flows. The policy question is not simply whether banks can keep customer-facing relationships. It is also which entities can observe transaction-level data, under what legal basis, with what partitioning, and with what protections against function creep as new use cases are added.

The striking part is that this concern is not new inside the Bank of Korea’s own work. In its 2023 paper, A step toward new financial market infrastructure: Bank of Korea’s initiative, the central bank explicitly devoted a section to personal information protection. That document said privacy standards should prioritize user confidentiality, described ongoing work on governance and privacy-enhancing technologies, and warned that privacy safeguards have to be balanced against system performance. In other words, the institution has already acknowledged that data protection is a first-order design variable, not a side note.

That gap between prior research and the latest public narrative is why Project Hangang deserves close attention from the broader RWA market. Around the world, tokenized funds, tokenized deposits and regulated stablecoins are converging on the same set of market-structure questions: who issues the money instrument, who controls the ledger, how delivery-versus-payment is finalized, and how sensitive financial data is segmented across operators. South Korea is effectively testing one possible answer — a bank-led tokenized deposit model anchored by central-bank settlement — but the experiment will carry more weight if the governance model is communicated as clearly as the technical stack.

For RWA builders, the lesson is straightforward. The next competitive frontier in onchain finance is not only token issuance or secondary-market access; it is trusted monetary infrastructure. Korea’s pilot shows how quickly tokenized cash, regulated intermediaries and programmable settlement can move from theory into production-like environments. It also shows that once these systems approach real economic scale, privacy, data rights and institutional accountability become product requirements, not afterthoughts. If Project Hangang can answer those questions convincingly, it will matter far beyond CBDC policy circles.