Europe’s MiCA endgame is turning from licensing headlines to operational cutover

With MiCA’s EU-wide transition expiring on 1 July, the immediate question is no longer who plans to get licensed, but which firms can finish client migration, custody transitions and wind-down execution on time. ESMA’s own statements and interim register show the market entering a hard compliance sorting event rather than a symbolic policy milestone.

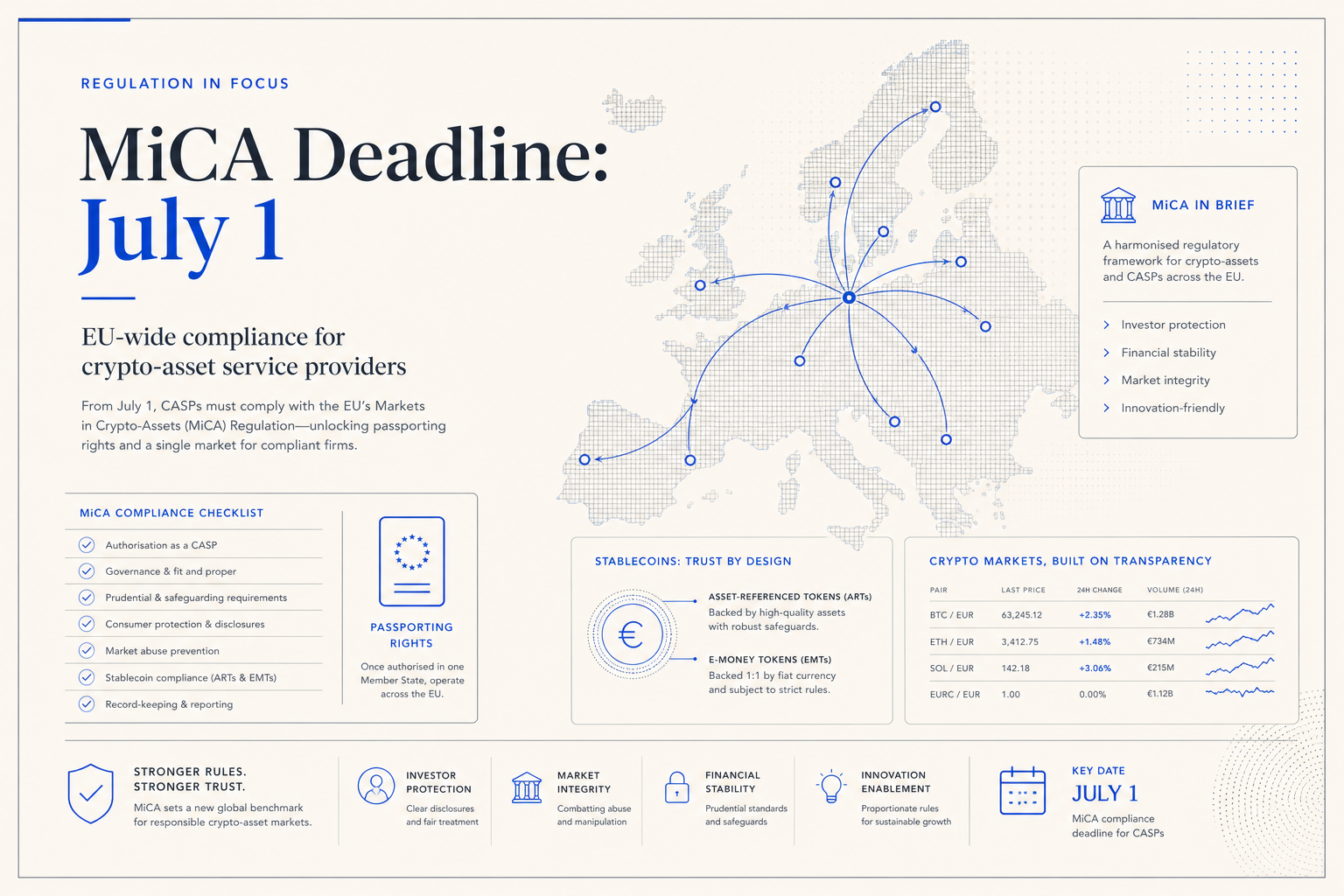

Europe’s crypto market is entering the final operational phase of MiCA, and the most important shift is no longer rhetorical support for regulation. It is execution. A fresh wave of coverage around the 1 July deadline has focused attention on what happens when the EU-wide transition ends, but ESMA’s own guidance makes the practical stakes clearer: once that date passes, any firm still providing crypto-asset services to EU clients without a MiCA licence will be in breach of EU law and is expected to have already put its wind-down plan into effect. For the market, that turns MiCA from a compliance roadmap into a live cutover event for exchanges, brokers, custody providers and the tokenized-asset distribution stack built on top of them.

The key document is ESMA’s 17 April 2026 statement on the end of transitional periods under MiCA. In that statement, ESMA said the transitional period will expire across the EU on 1 July 2026 and stated that unauthorised crypto-asset service providers must cease offering services after that date. Just as important, the regulator said wind-down plans should be operational, credible and immediately executable, including client offboarding and transfer arrangements where needed. That is a stricter message than a generic licensing reminder. It means firms that fail to secure authorisation are not supposed to improvise after the deadline; they are supposed to arrive at the deadline with a working exit plan already prepared.

The interim MiCA register gives a useful snapshot of how much of the market has made that transition and how much still sits outside the authorised perimeter. Using the register published by ESMA and updated on 12 June, there were 216 entries for authorised crypto-asset service providers, 40 entries for e-money token issuers, no entries for asset-referenced token issuers, and 149 entries listed under non-compliant entities. Those figures do not tell the whole story, because passporting, group structures and multiple service permissions can complicate the count. But they do show that MiCA is no longer an abstract future regime. Europe now has a visible authorised set, a visible warning list and a narrowing window for firms that have not completed the move.

That matters for users because the real friction is operational, not conceptual. ESMA’s statement says firms without authorisation should be able to offboard clients, transfer assets where appropriate and give prior notice before executing their wind-down plans. Authorised firms, meanwhile, are expected to actively manage migration of existing clients before the deadline and to apply full onboarding and AML controls in the process. In practical terms, that points to a short-term period of account notices, entity migrations, new terms of service, repeated KYC checks and possible market exits in jurisdictions where businesses cannot bridge the transition cleanly. The deadline may therefore feel less like a single legal switch and more like a staggered customer-experience event across the European market.

The cross-border message is equally important. ESMA reiterated that firms established outside the EU cannot provide MiCA-regulated services into the bloc except under a narrow reverse-solicitation exception, and it also warned against custody or service arrangements that effectively route EU client activity through unauthorised third-country entities. That point goes beyond spot crypto trading. It directly affects the distribution rails that many tokenization and stablecoin projects depend on, especially where issuance, custody, brokerage, treasury management and client servicing are split across multiple legal entities. MiCA’s endgame is therefore testing not just whether a product exists, but whether the full servicing chain behind that product can stand up inside the authorised perimeter.

For RWA markets, this is where policy becomes infrastructure. Europe has spent the last year building momentum around tokenized funds, digital bonds, tokenized deposits and regulated stablecoin issuance, but those products still need compliant access channels to reach users and institutions. If the brokerage, exchange, custody or transfer layer serving European clients is interrupted, product availability can narrow even when the asset itself remains sound. Stablecoins are especially exposed because they sit at the junction of payments, exchange funding, collateral management and onchain settlement. The same regulatory tightening that removes weaker service providers can also strengthen the case for better-capitalised operators that are willing to treat licensing, onboarding and reporting as product features rather than overhead.

The next two weeks should therefore be read less as a countdown to a political milestone and more as a market-structure stress test. Firms that have already secured authorisation or built compliant migration paths should emerge with a stronger distribution position inside Europe. Firms that relied on transitional ambiguity, fragmented entities or offshore servicing arrangements may find that the deadline closes faster than expected. For investors, tokenization teams and stablecoin operators, the lesson is straightforward: MiCA’s first real competitive filter is not whether Europe likes digital assets in theory. It is whether the firms carrying those assets to market can keep operating on 2 July with the same clients, the same balances and a regulator-ready operating model.