Ethereum’s selloff is no longer a clean read-through for the stablecoin economy

Ethereum’s June drawdown is exposing a structural shift in digital-dollar markets: stablecoin usage is spreading across multi-chain and bank-grade distribution rails even as ETH itself comes under pressure. The result is a less direct link between Ethereum market sentiment and the growth path for institutional stablecoins.

Ethereum’s June decline would once have been read as a direct warning sign for the broader stablecoin complex. That link is weaker now. Even as ETH came under pressure this month and debate intensified around competition, valuation and network direction, the infrastructure supporting digital dollars kept moving outward into a more diversified stack of issuer platforms, custody providers and tokenized cash rails. The market is starting to treat Ethereum’s price as one signal within the stablecoin economy rather than the signal.

That distinction matters because Ethereum still sits at the center of crypto financial history. It is where programmable smart contracts gave stablecoins their first real operating environment, where decentralized finance scaled, and where tokenized assets proved they could behave like software as much as securities or cash instruments. Recent reporting noted that ETH fell roughly 25% in June amid an organizational restructuring, workforce reductions and a new spending reset. Under an earlier market structure, that kind of drawdown would have cast a broader shadow over the long-term outlook for stablecoin adoption.

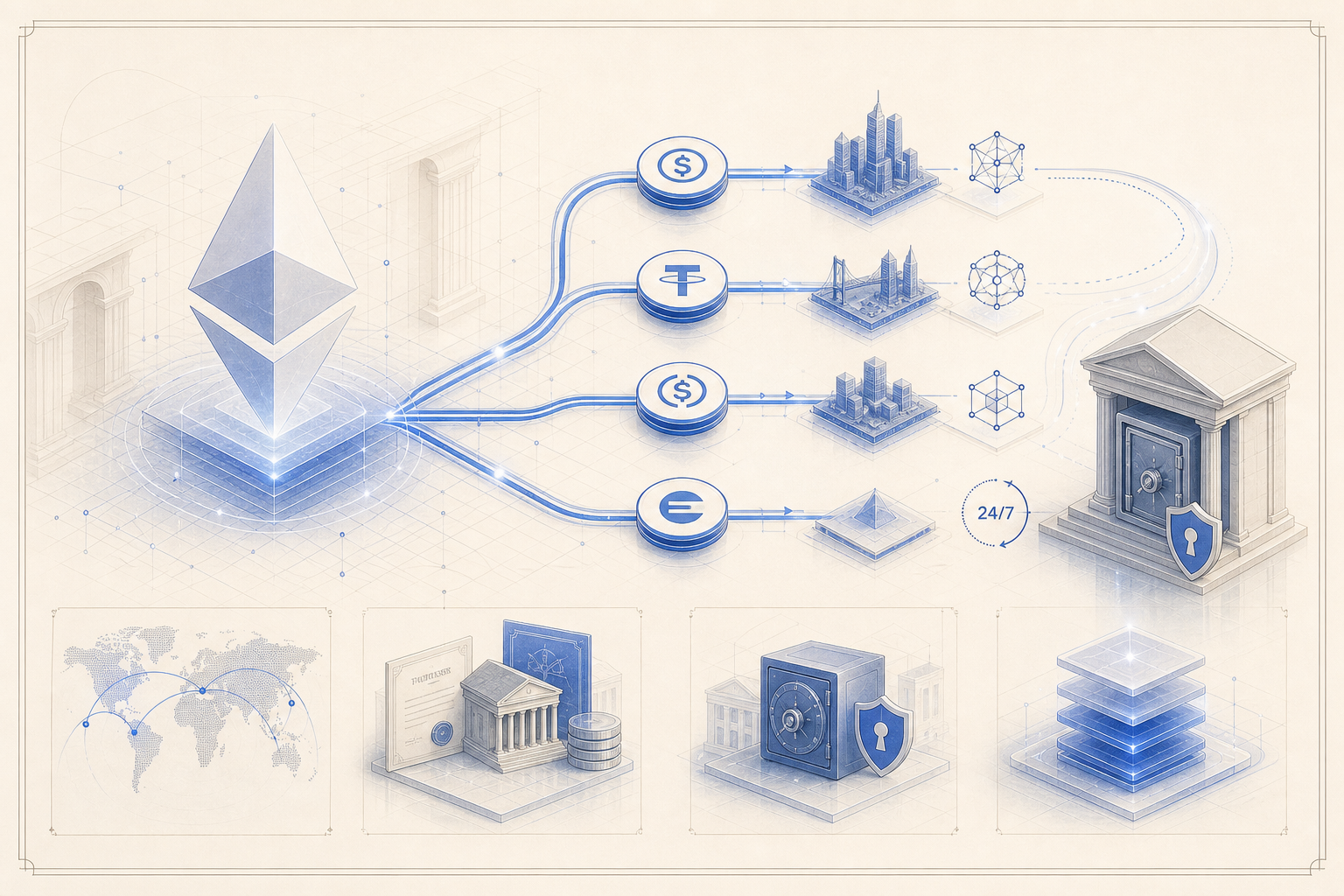

Instead, the latest cycle is showing how much the stablecoin stack has outgrown any single chain. Circle’s current USDC product materials say the token is natively issued across more than 30 blockchain networks and remains redeemable one-to-one for U.S. dollars. Circle also positions its Mint product specifically for exchanges, institutional traders, banks and other large financial institutions that need direct mint and redemption access rather than retail exchange exposure. That is an important change in market architecture: the center of gravity is shifting from a single base layer to a distribution model where the issuer relationship, compliance wrapper and redemption pathway matter at least as much as the chain where the token settles.

The same pattern is visible across institutional infrastructure. BNY’s digital-assets platform describes an always-on environment built to connect traditional finance with tokenization, custody, liquidity and digital payments, while its custody materials emphasize unified servicing across digital and traditional assets. J.P. Morgan’s Kinexys platform similarly frames blockchain more as programmable financial plumbing than as a standalone crypto venue, highlighting near-real-time money movement, tokenized money market funds and around-the-clock settlement. Taken together, those products point to a future in which institutions choose stablecoin rails based on operational resilience, interoperability, treasury control and compliance posture rather than loyalty to one public network.

That does not mean Ethereum is becoming irrelevant. It still offers deep liquidity, a mature developer base and a battle-tested settlement environment for sophisticated financial applications. But its role is changing. The more stablecoins become treasury instruments, settlement assets and regulated cash equivalents for enterprise workflows, the less end users care which chain provides the final execution layer. For a payments company or treasury desk, the critical questions are whether a token can move at all hours, whether it can be redeemed cleanly, whether custody is bank-grade and whether liquidity is available across counterparties and jurisdictions. Ethereum remains part of that answer, but it no longer monopolizes it.

This is why Ethereum weakness and stablecoin strength can now coexist. The stablecoin buyer in 2026 is not only a crypto-native trader parking capital between risk positions. It is also a payments operator, a treasury team, an exchange treasury desk, a fintech distributor and increasingly a bank or asset manager evaluating tokenized cash infrastructure. Those users care about programmability, but they care even more about settlement certainty and distribution efficiency. As issuers launch on more chains and institutions integrate direct mint-redeem workflows, the economic value of stablecoins becomes less dependent on ETH performing well as an investable asset.

There is a second implication for RWA markets. Tokenized treasuries, tokenized deposits and digital collateral systems all need cash-like settlement assets that can move continuously. If stablecoins are being abstracted away from one dominant network and into a multi-chain service layer, then the RWA sector gains optionality. Asset issuers can optimize for custody, compliance and user access without forcing every product decision through the same blockchain bottleneck. That may ultimately matter more for institutional adoption than any one month of ETH price action.

The cleanest conclusion is that Ethereum is still foundational, but no longer singular. Its downturn is important because it affects liquidity, sentiment and the economics of one of the industry’s core base layers. Yet the stablecoin economy now rests on a wider foundation that includes multi-chain issuance, direct redemption infrastructure and bank-connected operating rails. For investors and operators alike, that means ETH’s price can still influence the conversation without defining the destination.