DTCC moves tokenized securities into live market workflows as Wall Street pilots production trading

DTCC has taken tokenized securities out of the lab and into live production-style market workflows, with major banks and asset managers testing equities, ETFs and Treasuries across collateral, margin and settlement flows. The milestone matters because it puts blockchain-based representations of regulated securities inside the core plumbing institutions already use.

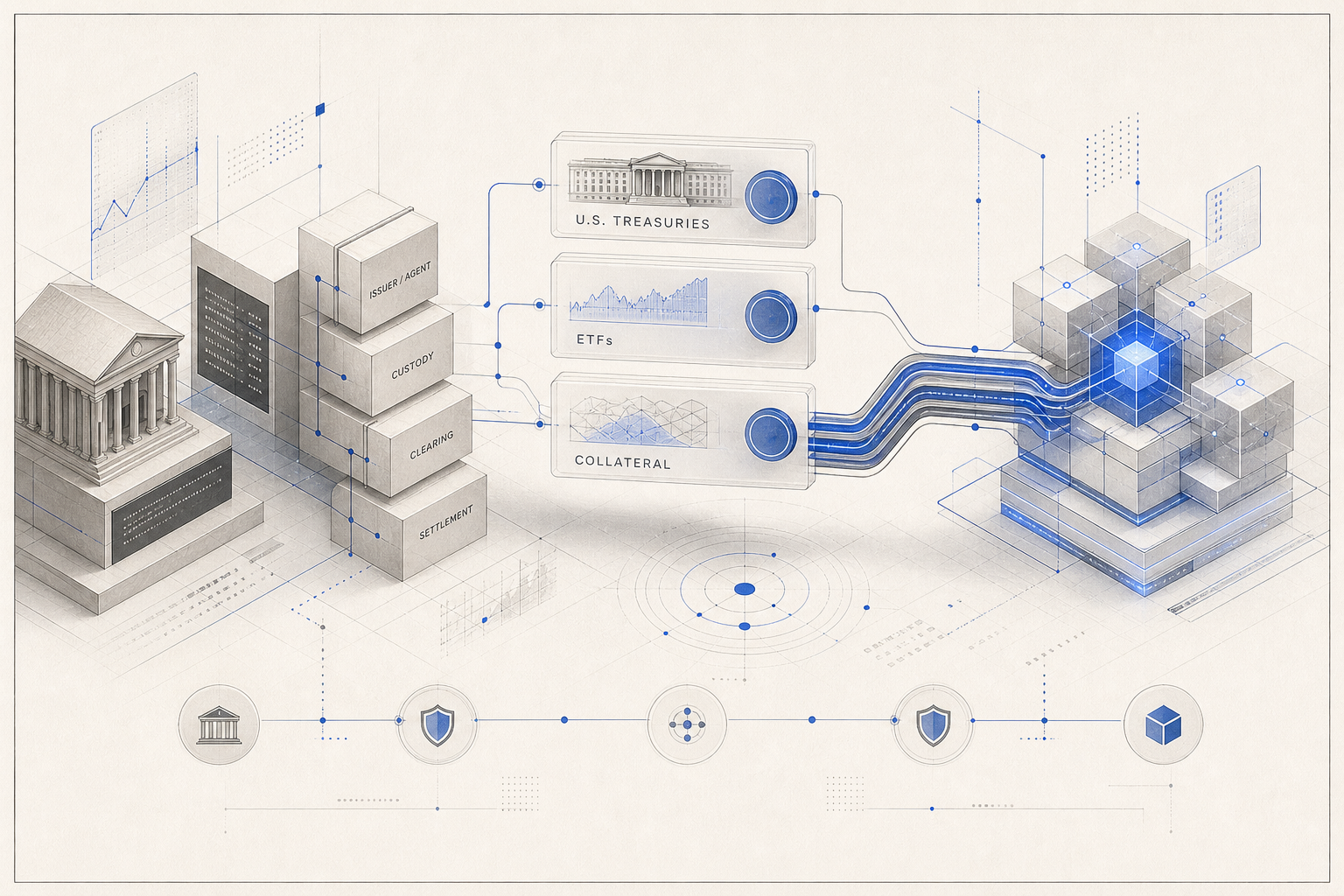

DTCC has moved tokenized securities into live transaction flows, giving the market one of its clearest signals yet that blockchain-based asset rails are being tested inside the existing infrastructure of U.S. capital markets rather than around it. The latest production event brought together more than two dozen large institutions, including global banks, asset managers and market infrastructure providers, to process transactions involving tokenized equities, exchange-traded funds and U.S. Treasuries. The exercise covered collateral transfers, repo activity, margin movements, securities trades and broader asset-transfer workflows, showing that tokenized instruments are now being handled in operating environments that resemble the real conditions of institutional post-trade markets.

What makes the event notable is DTCC’s position in the market stack. Its depository and clearing infrastructure sits at the center of how traditional securities ownership is recorded, serviced and settled, so a live tokenization workflow there carries different weight from a standalone crypto venue or a limited sandbox pilot. In this case, the assets used in the exercise were already held within DTC’s custody framework and then represented on blockchain rails as digital versions tied back to the underlying securities. That structure is important because it keeps the tokenized representation anchored to the legal and operational framework institutions already recognize, rather than creating a separate wrapper whose rights may differ from direct ownership.

The production run also expanded the discussion beyond theory into specific use cases. Market participants used tokenized collateral to satisfy margin requirements, processed Treasury-related transactions onchain and demonstrated how tokenized ETF positions could move through broader market plumbing. One example involved the conversion of ETF holdings into tokenized form before those assets were used in a margin workflow with CME Group. Other activity included tokenized equity transfers and collateral pledges. In practice, that means the test was not just about issuing a token against a familiar security; it was about showing whether tokenized forms can support the high-friction institutional tasks that matter most for funding, collateral mobility and balance-sheet efficiency.

The technical setup also points to the direction of travel for regulated tokenization infrastructure. Some of the transactions were processed on Hyperledger Besu, while others used the Canton Network, which was designed for regulated financial institutions that need privacy controls while still sharing synchronized data across participants. That interoperability matters because large financial firms are unlikely to migrate critical market activity onto a single public stack overnight. Instead, the practical path is likely to involve tokenized assets moving across multiple permissioned or hybrid environments, with institutions preserving compliance, confidentiality and operational resiliency while gradually reducing reconciliation and transfer friction.

This week’s activity did not emerge in isolation. In December, DTCC, Digital Asset and the Canton Network said they were partnering to tokenize a subset of DTC-custodied U.S. Treasury securities, with an initial minimum viable product targeted for a controlled production environment in the first half of 2026 and a wider expansion dependent on client demand. Digital Asset said at the time that the program followed SEC no-action relief for a DTCC service covering tokenized, DTC-custodied real-world assets. That earlier roadmap matters because it showed DTCC was not treating tokenization as a marketing experiment. The live workflows now suggest the project has moved from architectural planning into operational proving ground.

For the broader RWA market, the biggest implication is not that every security is about to trade onchain tomorrow. It is that tokenization is being tested where institutional bottlenecks are most expensive: collateral movement, margining, settlement coordination and asset servicing across multiple firms. Those are areas where traditional market structure still depends on fragmented ledgers, operating cutoffs and reconciliation-heavy handoffs. If tokenized representations can move through those processes while preserving the legal status of the underlying securities, the benefit is less about novelty and more about compressing time, reducing trapped collateral and improving capital efficiency.

That framing also helps explain why Wall Street’s tokenization efforts increasingly center on Treasuries and fund interests rather than speculative retail instruments. Short-duration government paper, cash-like funds and institutionally held securities are easier starting points because they already sit inside well-defined custody, compliance and servicing regimes. Products such as BlackRock’s BUIDL, Ondo’s OUSG and OpenEden’s TBILL have already helped establish investor familiarity with tokenized fixed-income exposure onchain. DTCC’s latest work pushes the market one layer deeper, toward a future where tokenization is not just an issuance format but part of the everyday operating system for collateralized finance.

The remaining question is adoption at scale. A successful live demonstration shows that the rails can work, but broad usage will depend on which securities become eligible, how participants measure operational savings, what regulators permit and whether clients are willing to shift meaningful flows into tokenized form. Even so, the latest DTCC event marks an important threshold for RWA infrastructure. The center of gravity is moving from proofs of concept around the edges of finance toward production-grade experiments inside the institutions that already run the market.