Bank-Led Tokenized Deposits Move Closer to Treasury and Cross-Border Payment Workflows

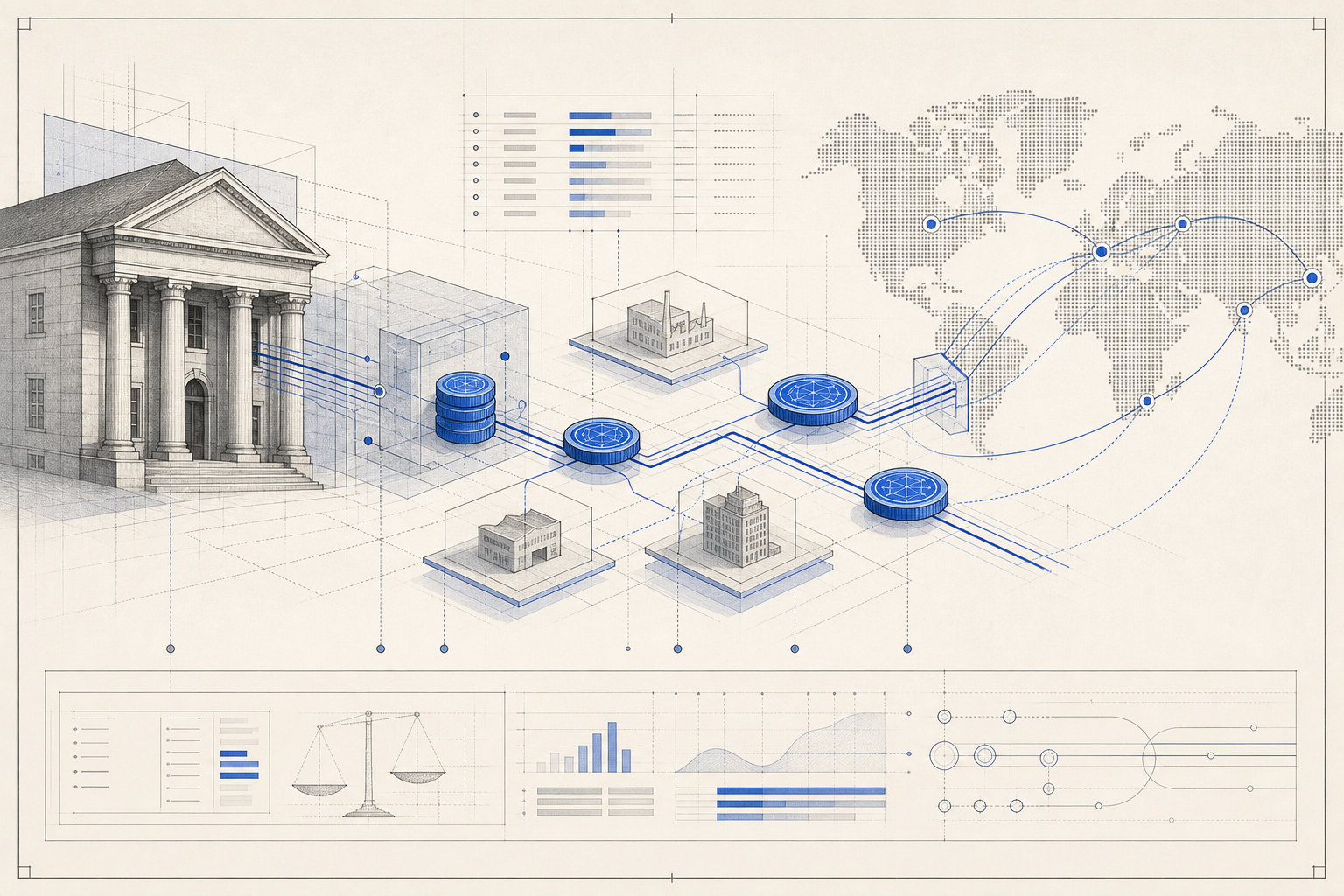

Banks are sharpening the commercial case for tokenized deposits around corporate treasury, cross-border settlement and automated liquidity management rather than consumer-facing crypto payments. Recent disclosures from The Clearing House, large bank payments teams and existing tokenized-deposit platforms suggest the first real scaling path is institutional cash movement inside the regulated banking perimeter.

The latest turn in the digital-dollar race is becoming more specific. Instead of framing tokenized deposits as a vague response to stablecoins, banks are now describing where they think the product can win first: corporate treasury, cross-border business payments and software-driven liquidity management. That matters for the RWA market because the most durable adoption usually appears where a blockchain-based instrument solves an operational problem inside an existing financial workflow, not where it simply creates a new wrapper for money. Recent reporting from PYMNTS, combined with fresh disclosures from major bank infrastructure providers, points to a market that is moving from conceptual pilots toward a clearer institutional operating model.

The immediate backdrop is the June 5 announcement of a bank-led onchain money initiative operated by The Clearing House. The project is designed to connect blockchain-based activity with established bank payment rails and support clearing and settlement for tokenized commercial bank money at scale. In its own announcement, The Clearing House said the network is meant to support tokenized-deposit settlement between banks, richer transaction data, automated workflows and around-the-clock settlement within the regulated banking framework. The organization also listed the commercial use cases it sees as most relevant: programmable treasury operations, real-time liquidity management, cross-border payments, digital asset settlement and agentic commerce. That is a much more practical roadmap than the earlier industry habit of describing tokenized deposits as a generic innovation theme.

The follow-on discussion reported by PYMNTS pushed that operating thesis further. Executives speaking around The Clearing House media day argued that multinational treasury teams and cross-border B2B flows are emerging as the most credible early deployment areas. The logic is straightforward. Large corporates already struggle with trapped cash, cut-off times, fragmented banking hours and slow visibility across legal entities and jurisdictions. A tokenized deposit system that remains inside the banking system can, in principle, add programmability and continuous settlement without forcing treasurers to leave familiar regulatory and credit structures behind. That makes the product easier to position as an enterprise infrastructure upgrade rather than a new asset class that finance teams must underwrite from scratch.

Primary-source materials from participating banks reinforce that interpretation. J.P. Morgan’s Kinexys platform presents blockchain-based deposit accounts and programmable payments as a way to bridge legacy and digital financial systems with 24/7 money movement, near-real-time settlement and tokenized asset servicing. The same product stack also points to adjacent use cases such as tokenized money market funds and onchain collateral flows, which is important because treasury modernization rarely happens in isolation. Once institutions can move balances continuously and attach rules to cash, the next step is usually to integrate that capability with short-duration yield products, internal funding decisions and collateral mobility. In other words, tokenized deposits are not just about faster payments; they are about turning bank money into software-addressable working capital.

Another important corroborating signal came from DBS and Kinexys last year, when the two banks said they were developing an interoperability framework for interbank tokenized-deposit transfers across multiple blockchains. DBS said the goal was to enable exchangeability and settlement across public and permissioned networks while preserving real-time, round-the-clock availability for clients. That announcement matters because interoperability is one of the core bottlenecks for tokenized bank money. A tokenized deposit is only strategically valuable if it can move beyond a single institution’s walled garden and still preserve settlement certainty, singleness of money and compliance controls. The fact that large banks are already working on that layer suggests the market is thinking past internal proofs of concept and toward network effects.

This is also where tokenized deposits begin to intersect more directly with the wider RWA stack. The Clearing House announcement explicitly referenced tokenized securities momentum and noted that Citi Token Services is already live and operating at scale. As tokenized Treasuries, money market products and other onchain representations of traditional financial assets continue to grow, institutions need a native cash leg that can settle inside the same operating environment. Stablecoins have filled part of that role, especially in crypto markets, but banks are making the case that deposit tokens can serve treasury and credit-sensitive use cases without moving balances outside the commercial banking system. For RWA infrastructure builders, that distinction matters: the winning architecture may not be stablecoins versus tokenized deposits, but a market where each serves different layers of institutional settlement.

There are still meaningful execution questions. Banks will need shared standards, operating rules, legal clarity and enough interoperability to avoid a fragmented patchwork of deposit networks. Treasurers will also demand hard evidence that tokenized workflows improve visibility, shorten funding cycles and reduce operational friction in measurable ways. But the direction of travel is becoming clearer. The strongest near-term opportunity is not retail adoption or speculative trading. It is the quiet rebuilding of wholesale money movement around programmable bank liabilities that can plug into onchain asset markets and enterprise treasury software. If that thesis holds, tokenized deposits may become one of the most important connective layers between traditional banking infrastructure and the next phase of RWA settlement.