Backpack Pushes Tokenized Equities Toward Exchange-Native 24/7 Market Structure

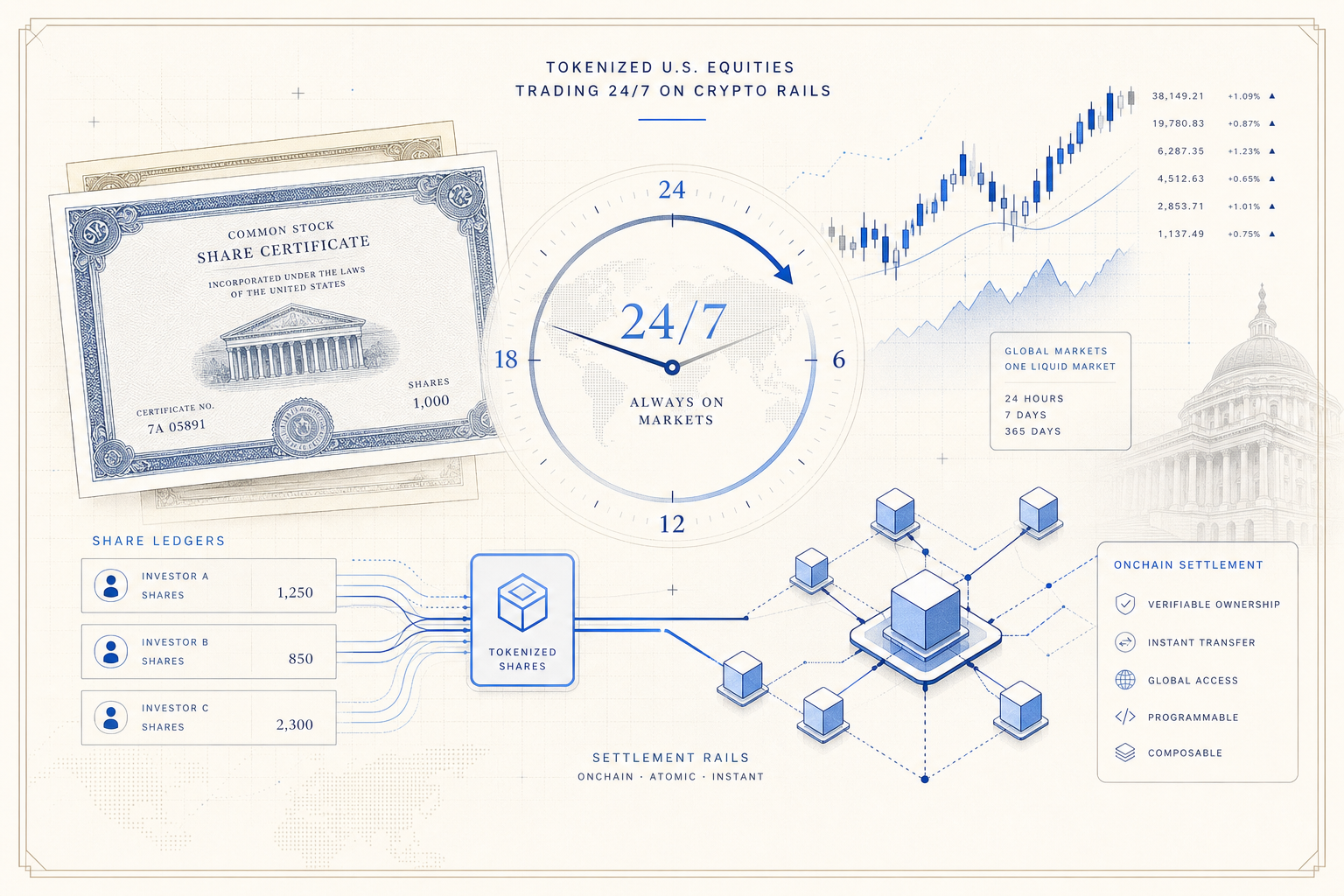

Backpack has opened round-the-clock trading in a limited set of tokenized U.S. equities, pairing exchange order books with onchain transferability. The launch matters because it tests whether tokenized stocks can evolve from niche wrappers into exchange-native market infrastructure with stablecoin settlement and wallet portability.

Backpack has launched 24/7 trading for a first batch of tokenized U.S. equities, adding another serious test case for whether blockchain-based stock products can become more than a marketing layer around traditional securities. The immediate headline is straightforward: international users can now trade selected names including SpaceX, Micron and SanDisk at all hours through a crypto exchange interface. The more important signal for the RWA market is structural. Backpack is combining exchange-style access, stablecoin-based funding paths and onchain portability into a single product, which is much closer to a live market stack than the earlier wave of tokenized equity experiments built around limited hours or synthetic exposure.

According to Backpack’s launch details reported by Cointelegraph, the initial product is available to investors in more than 150 countries and regions and starts with a relatively narrow list of U.S. equities rather than a full stock shelf. Backpack said users receive direct ownership of the underlying securities instead of a synthetic claim, and that trades settle instantly while accounts can be funded in either fiat currency or stablecoins. That combination is notable because tokenized stock projects have often had to choose between crypto-native usability and familiar capital-markets design. Backpack is trying to present both at once: exchange execution for retail-style users and a tokenized representation that can move across wallets and onchain applications.

The operating design matters as much as the availability claim. Backpack said the tokenized versions of these equities are issued on Solana, can be transferred wallet to wallet, can be used in DeFi applications and can be converted 1:1 into the corresponding shares through the platform. If that process works cleanly in production, it creates a more credible bridge between offchain securities custody and onchain utility than many prior tokenized stock offerings. It also frames tokenized equities less as a derivative side product and more as a settlement and distribution format for securities that can circulate in multiple contexts. That distinction is central to the long-term RWA thesis, where the value is not only digitizing the asset but also improving how it trades, settles, moves and integrates with programmable financial rails.

Backpack’s own market data pages support the view that this is already being wired into a live exchange environment rather than held back as a concept launch. The company’s public market-info assets page shows open spot markets quoted against USDC for symbols including SPCX.US, MU.US and SNDK.US. Those listings indicate tokenized stock pairs are being treated as exchange instruments with visible market metadata, not merely as static product pages. The same public pages also show creation timestamps for those markets in late June and early July, suggesting Backpack has been staging the rollout over several weeks before broadening its 24/7 access narrative. In practice, quoting these products against USDC is one of the clearest signs that the company expects stablecoins to function as a core settlement leg for tokenized equity trading.

Additional issuer-side corroboration comes from xStocks, whose product catalog lists SPCXx, MUx and SNDKx and describes its tokenized equities and ETFs as 1:1 backed, compliant and DeFi-ready. The xStocks products page says its instruments provide onchain exposure to major equities while remaining backed one-for-one by the underlying security, and it links users to legal documentation hosted by backed.fi. That does not remove the offchain dependencies inherent in a tokenized stock model, but it does clarify that Backpack’s launch is sitting on top of a broader issuance and legal wrapper framework rather than inventing its own isolated product format from scratch. For the RWA market, that is a more important development than a simple volume milestone because it points to reusable issuance plumbing that other exchanges and applications could tap.

This is also happening at a moment when tokenized equities are moving from peripheral curiosity to one of the faster-growing segments of onchain finance. The market’s recent growth has attracted both crypto exchanges and traditional trading venues because equities solve a different problem from tokenized Treasury products. Instead of focusing mainly on collateral efficiency or parked cash yield, tokenized stocks address distribution and market structure: who can trade, when they can trade, what they can use for settlement and whether those positions can interact with other onchain systems. A 24/7 exchange model directly targets that opportunity. If users can buy stock exposure with stablecoins, move positions onchain and potentially deploy them elsewhere, the product starts to resemble a programmable capital-markets rail rather than a closed brokerage account with crypto branding.

The harder questions are still ahead. Tokenized equities must prove that liquidity remains resilient outside U.S. market hours, that corporate actions and issuer disclosures are handled cleanly, that redemption and conversion workflows are understandable, and that jurisdictional access controls hold up under scrutiny. Those issues will determine whether the sector remains a small offshore growth pocket or becomes a durable category inside regulated digital-asset infrastructure. Even so, Backpack’s launch qualifies as a meaningful RWA milestone because it brings together direct-share framing, stablecoin settlement, onchain transferability and named public-equity products in a format users can actually trade. If the company can expand the roster, maintain depth and show that the token layer adds real utility rather than just novelty, tokenized equities will look increasingly like an infrastructure business and not just a speculative side market.