Archax pushes tokenized securities toward real-time income settlement on Hedera

Archax has launched a system on Hedera that streams yield from tokenized securities to investors’ wallets in USDC as ownership changes. The upgrade matters because it shifts tokenization from static issuance toward continuous, onchain handling of the cash flows those assets generate.

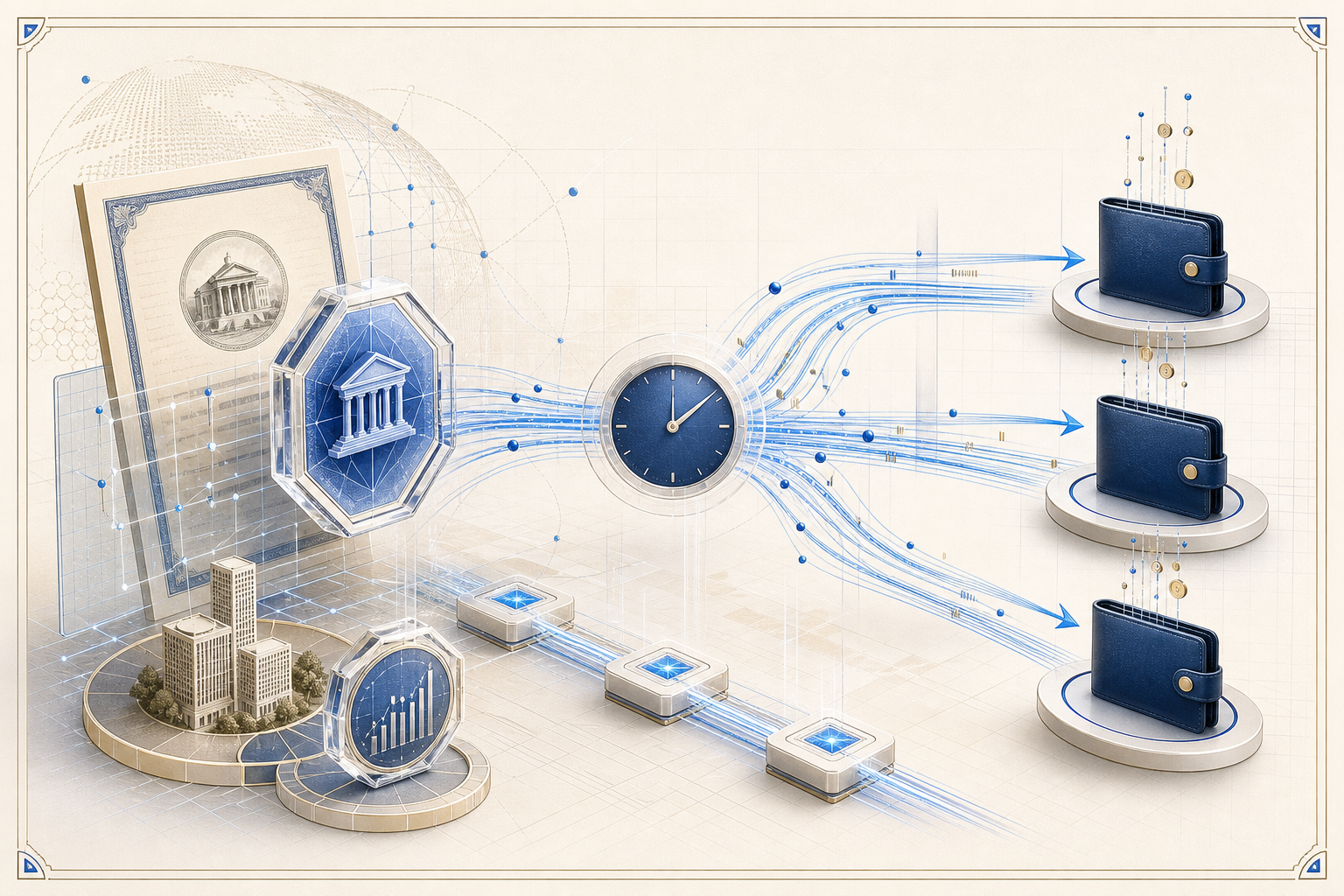

Archax is moving the tokenization conversation beyond issuance and into the mechanics of income distribution. The UK-regulated platform says it has launched real-time streaming cash flows for tokenized securities on Hedera, allowing interest to accrue directly into investors’ wallets in USDC on a near continuous basis. That may sound like a narrow product enhancement, but it addresses one of the most stubborn gaps between tokenized assets and their traditional equivalents: a token can move instantly onchain, while the coupon, yield or other cash entitlement tied to it often still depends on slower batch processes, record dates and post-trade reconciliation.

The core feature is that the cash flow is meant to follow the asset as ownership changes. Archax says that when a tokenized security moves between wallets, the associated interest stream adjusts in real time rather than waiting for a periodic payout cycle. Because the underlying securities can be fractionalized, the payment leg can also be divided with similar precision. In practical terms, that creates a model in which an investor’s economic exposure and their incoming cash flow stay synchronized onchain, reducing the mismatch that has historically made many tokenized products look modern at the transfer layer but conventional underneath.

This launch also builds on infrastructure Archax and Hedera were already developing for institutional tokenized funds. In September 2025, Archax introduced its Pool Token structure on Hedera, designed to wrap multiple tokenized assets into a single onchain basket. The first example was built as a portfolio of money market funds from Aberdeen, BlackRock, State Street and Legal & General. That earlier launch was important because it showed Archax was not only tokenizing single instruments, but also experimenting with portfolio construction and fund-like wrappers onchain. The new streaming-yield capability takes the next logical step by trying to modernize how those instruments distribute value after issuance.

Why that matters for the RWA market is straightforward. Tokenized treasuries and money market products have grown quickly because they offer familiar collateral quality with blockchain settlement characteristics. But yield-bearing products still inherit some of the operational plumbing of traditional funds, especially around cutoffs, transfer records and payout timing. A system that can update interest claims continuously makes tokenized securities more usable in secondary markets, because buyers and sellers do not need to manage as much uncertainty around who is entitled to the next payment and when that payment will settle. That is especially relevant if tokenized funds are expected to function as collateral, treasury instruments or building blocks in larger onchain portfolios.

The broader market context supports that direction. RWA Trails’ live catalog already shows deep institutional attention concentrated in onchain cash and treasury instruments such as BlackRock’s BUIDL, Franklin Templeton’s BENJI fund and Hashnote’s USYC. Those products have helped prove investor appetite for short-duration, yield-bearing assets onchain, but they also underline the next challenge for the sector: turning tokenized ownership into tokenized operations. Settlement speed has limited value if the associated income stream still behaves like an offchain spreadsheet exercise. Archax’s new design is an attempt to close that gap.

There are still reasons to stay measured. Real-time distribution creates new demands around accounting, wallet infrastructure, compliance controls and investor reporting, particularly when products move across jurisdictions or between institutional counterparties with different custody arrangements. It also remains to be seen how broadly issuers want to adopt continuous payment logic when many established securities workflows are built around periodic events and administrator oversight. For some products, daily or periodic distribution may remain operationally preferable even if second-by-second capability exists.

Even with those caveats, the direction is notable. The first phase of RWA tokenization proved that funds, bonds and other instruments can be represented onchain. The more important second phase is whether the rights attached to those instruments, including yield, can be administered natively onchain as well. Archax’s Hedera rollout is a credible step in that direction because it targets a real market inefficiency rather than a cosmetic feature. If tokenized securities are going to compete with conventional capital-markets infrastructure, they will need to improve not only how assets trade, but also how income moves. This launch is one of the clearest signs yet that the market is starting to work on that harder layer.